The Wheel Strategy FAQ: Everything You Want to Know Before You Start

The Wheel Strategy is one of the most practical ways to generate monthly income from a stock portfolio.

It’s simple enough to explain in a few sentences, disciplined enough to run for years, and conservative enough that you never need margin or leverage.

But most people who hear about it for the first time walk away with more questions than answers.

How much money do I need?

What kind of returns are realistic?

What actually happens when things go wrong?

This post answers the 10 most common questions people have when they’re just starting to explore the strategy.

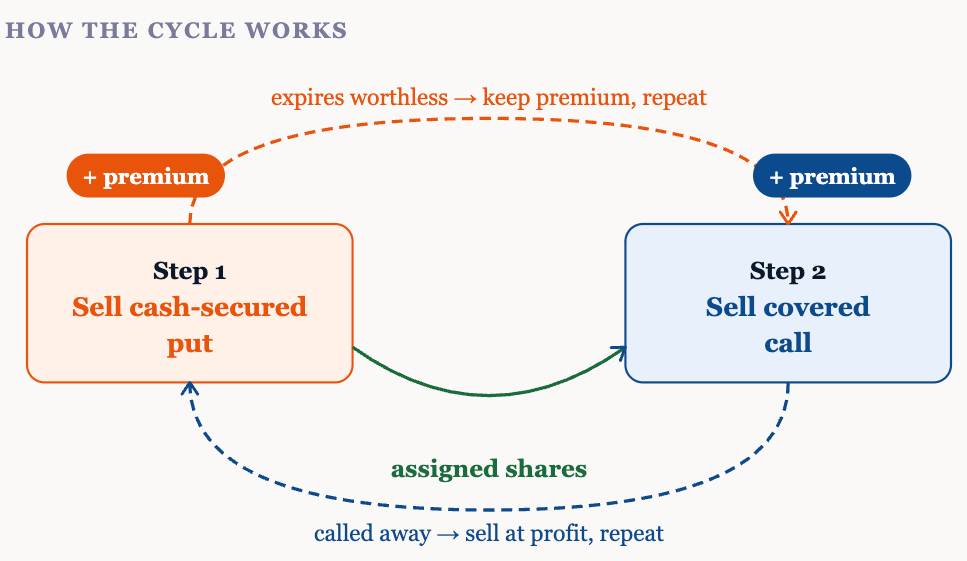

1. What is the Wheel Strategy?

The Wheel is a repeating two-step process for generating income from stocks you’d be comfortable owning.

Step one:

you sell a cash-secured put on a stock you like. This means you agree to buy 100 shares at a specific price (the strike) if the stock drops to that level. In exchange, you collect a premium upfront — cash in your account, immediately.

If the stock stays above your strike, the put expires worthless and you keep the premium. That’s it. You earned income for waiting.

Step two:

only happens if the stock drops and you’re assigned shares. Now you own stock you wanted anyway, at a price you chose, with a cost basis reduced by the premium you already collected. From here, you sell a covered call — agreeing to sell those shares at a higher price if the stock rises. You collect another premium.

If the stock gets called away, you’ve sold at a profit and your cash is free to start the cycle again.

The whole thing loops: sell puts, potentially own stock, sell calls, potentially sell stock, repeat.

Each step generates income.

The strategy works in sideways markets, slightly up markets, and even slightly down markets — which is most of the time.

For the full mechanical breakdown, see below:

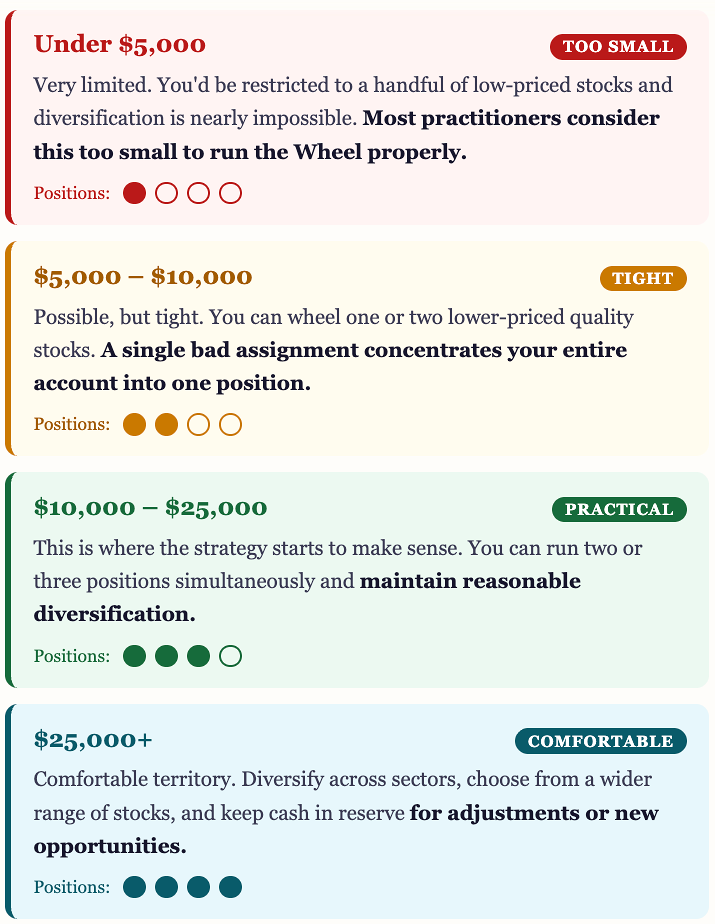

2. How much money do I need to start?

Because each options contract covers 100 shares, you need enough cash to buy 100 shares at your chosen strike price.

If you’re selling a put on a $50 stock, that’s $5,000 in collateral.

A $200 stock requires $20,000.

At different account sizes, here’s what’s realistic:

The deeper breakdown is below:

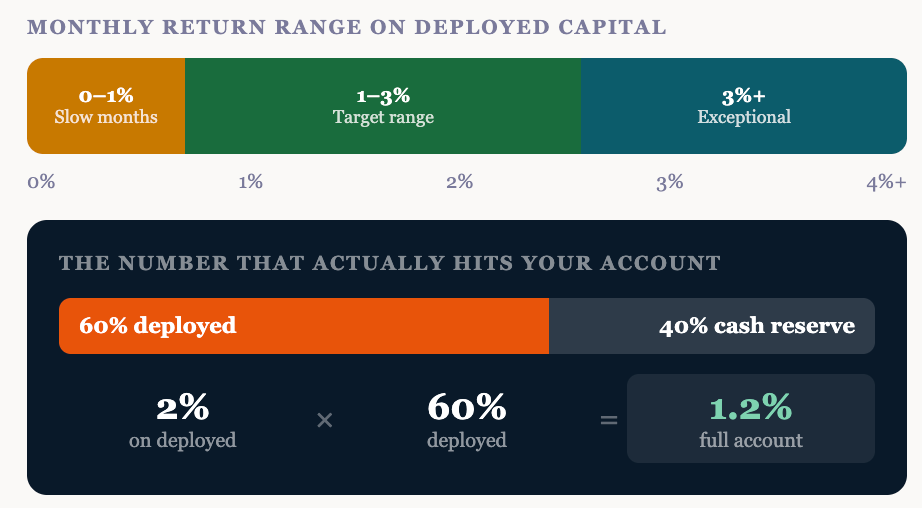

3. What kind of returns are realistic?

Most disciplined Wheel traders target 1–3% per month on deployed capital.

That’s roughly 12–36% annualized, depending on strike selection, stock choice, and market conditions.

An important distinction: those numbers are on deployed capital, not your whole account.

If you keep 40–50% in cash reserve (sound practice), the return on your total portfolio is lower. A 2% monthly return with 60% deployed translates to about 1.2% on the full account. Still solid — but different from the headline number.

Some months are easy.

Others — especially during strong rallies with thin premiums, or sharp drawdowns where your capital is tied up in assigned shares — will produce less. The Wheel won’t double your money in a year. A $100,000 portfolio producing $1,000–$2,000 per month in premium won’t make headlines, but over five or ten years the compounding is substantial.

One uncomfortable truth most Wheel educators skip: the strategy underperforms in a strong bull market. Covered calls cap your upside. If stocks rip straight up, buy-and-hold wins.

The Wheel earns its edge in sideways and moderately volatile markets — which is where markets spend most of their time.

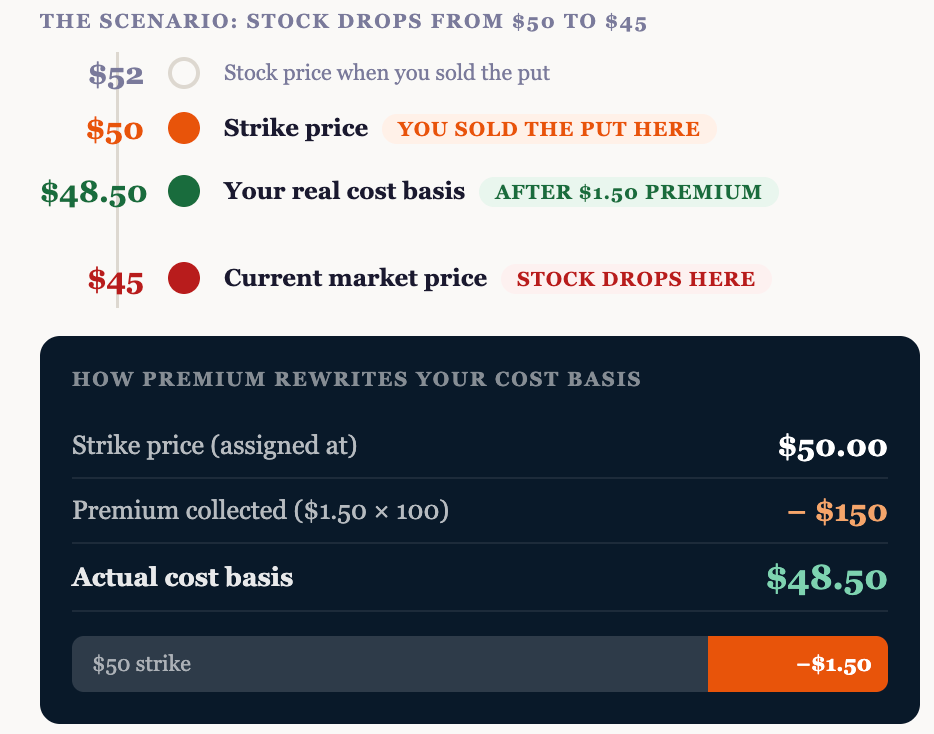

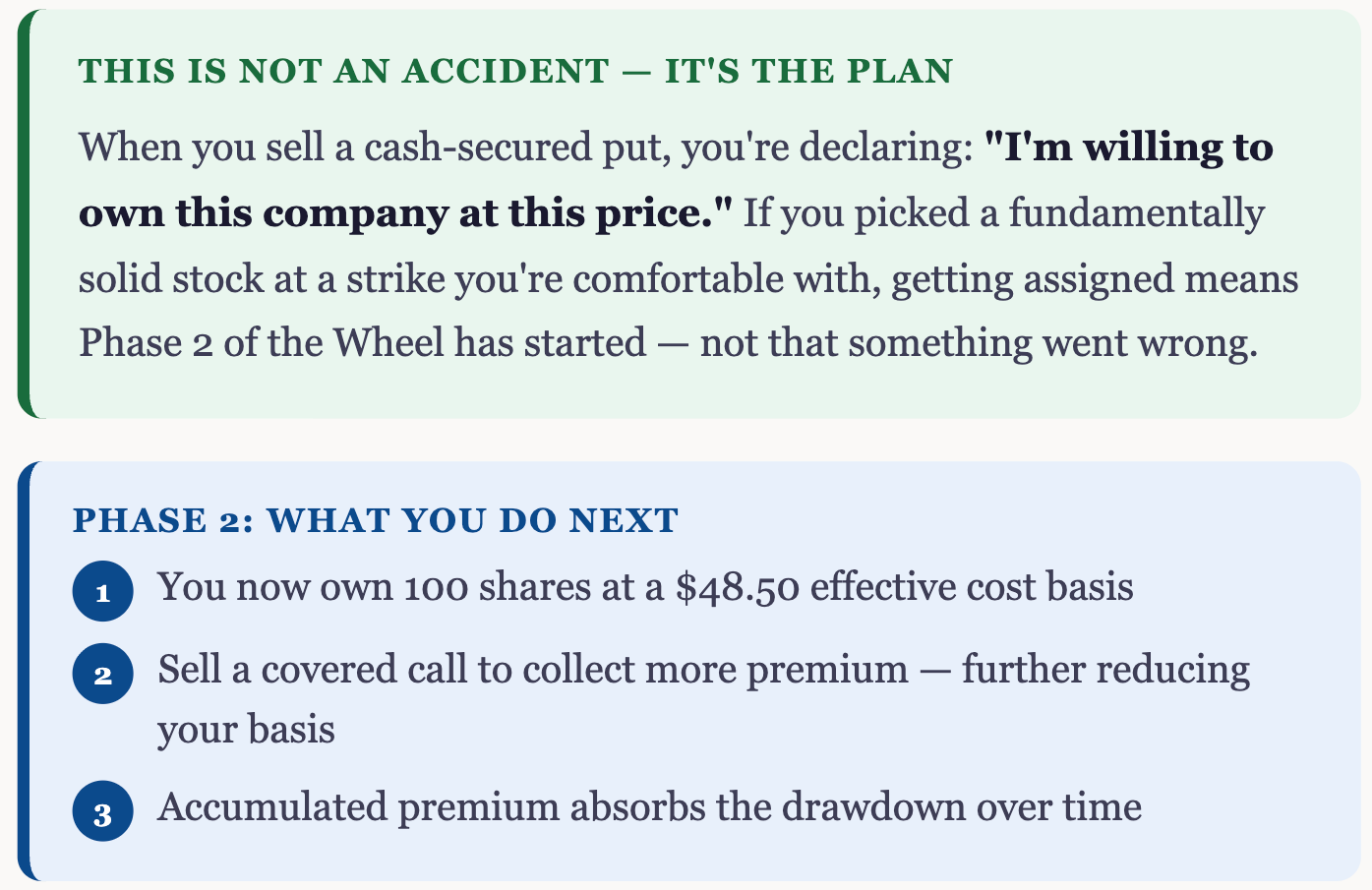

4. What happens if the stock drops after I sell a put?

This is the fear that stops most people from starting, so let’s use a concrete example.

You sell a put at a $50 strike and collect $1.50 per share in premium.

The stock drops to $45 and you’re assigned 100 shares.

That feels bad — but your actual cost basis isn’t $50.

It’s $48.50, because the premium you already collected reduces what you effectively paid.

The real danger isn’t assignment itself.

It’s being assigned a stock you didn’t actually want to own, or sizing the position too large for your account. Both are preventable.

For the full decision framework, see:

5. Is this better than just buying index funds?

They solve different problems.

Index funds are built for long-term capital appreciation.

The Wheel is built for monthly income.

They’re complementary, not competitive — and many investors run both.

The trade-off is straightforward: the Wheel caps some upside (covered calls limit gains beyond the strike) in exchange for premium income regardless of whether the stock moves.

In a year where the S&P rips 25%, buy-and-hold wins.

In a year where markets drift sideways, the Wheel trader is still collecting income while the index investor earned close to nothing.

The right question isn’t “which is better?” — it’s “what am I trying to accomplish with this capital?”

6. How much time does this take each week?

Less than most people expect.

This is not day trading.

A typical week: an hour or two on the weekend reviewing your watchlist and identifying setups. Fifteen to thirty minutes placing orders. A quick check on positions during the week — maybe 10 minutes a day. Most of the time, there’s nothing to do. The puts are either expiring worthless or moving toward assignment, both of which are planned outcomes.

The exception is during sharp market moves or when a position goes in-the-money, where you might spend 30–60 minutes evaluating your options.

But those situations don’t happen every week, and the decision framework is straightforward when they do.

Every Monday, this publication delivers 10–15 pre-screened Wheel setups with full execution plans. For paid subscribers, the stock screening and setup analysis is already done — which reduces the weekly time commitment further.

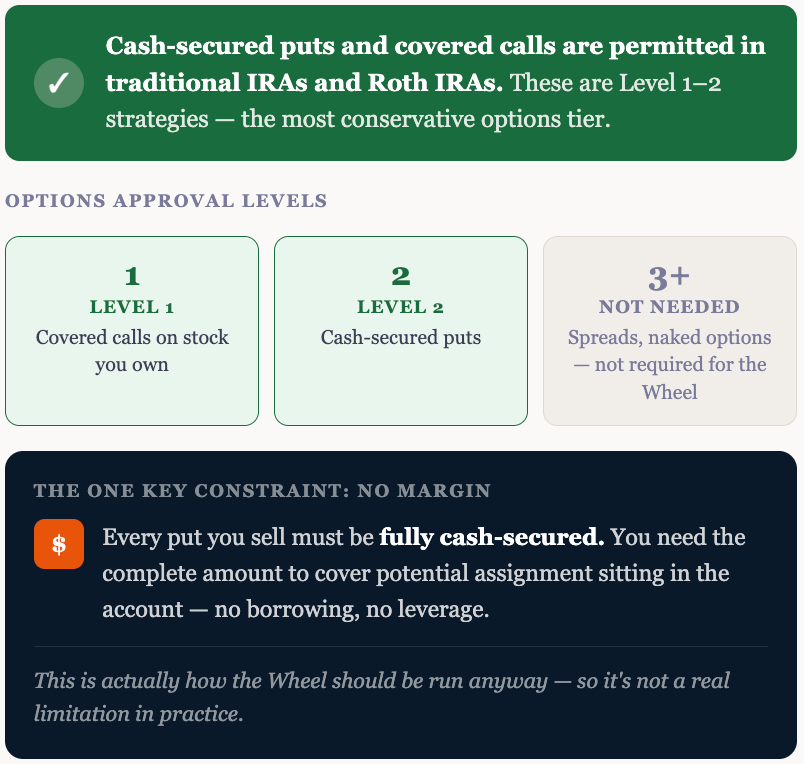

7. Can I do this in an IRA or retirement account?

Yes.

Most U.S. brokerages allow cash-secured puts and covered calls inside traditional and Roth IRAs. You’ll need to apply for options approval (typically Level 1 or Level 2), but the process is straightforward for these conservative strategies.

The key constraint: no margin in retirement accounts.

Every put must be fully cash-secured.

But that’s how the Wheel should be run anyway, so it’s not a real limitation.

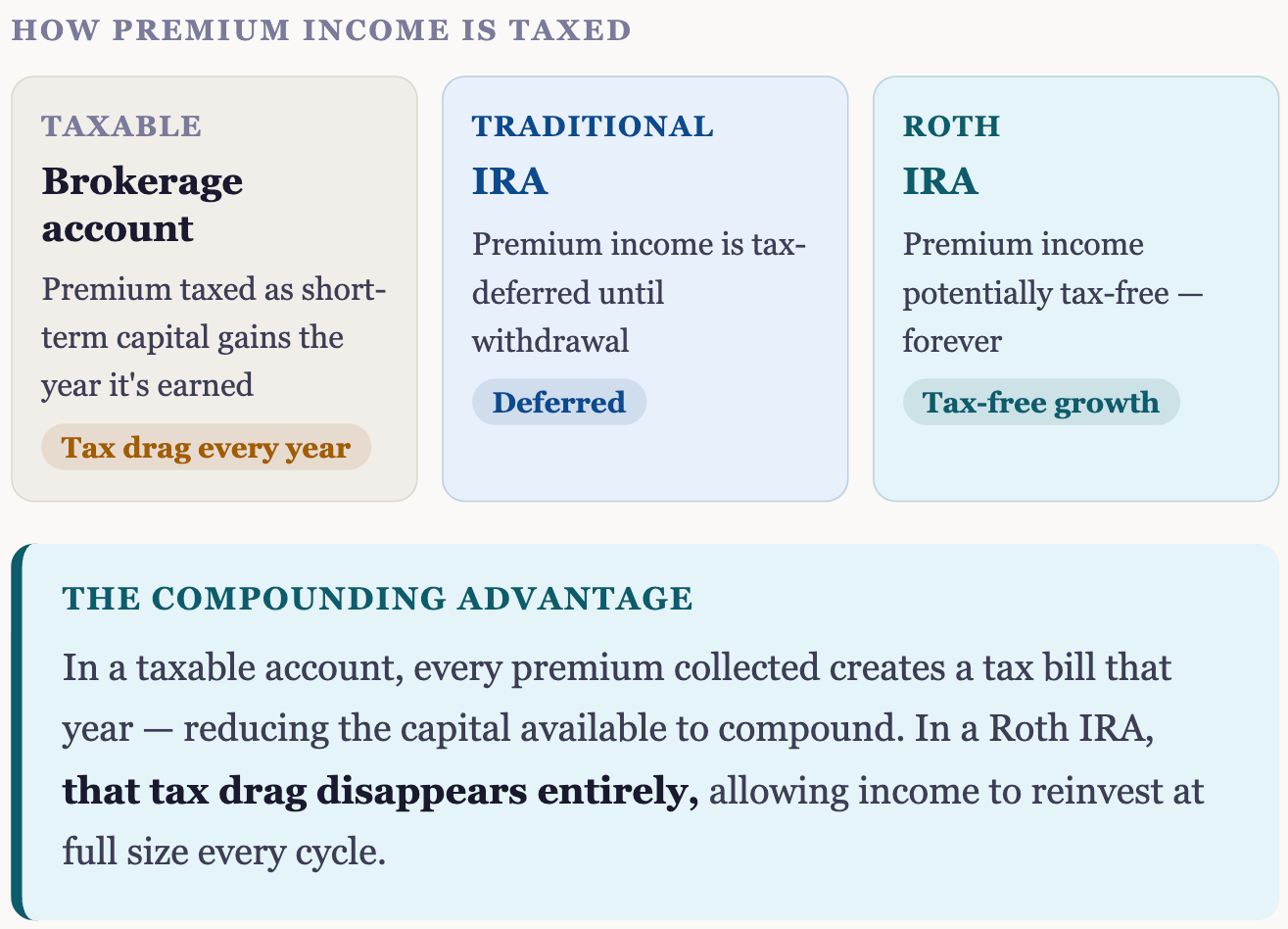

The advantage is meaningful. In a taxable account, option premiums are typically taxed as short-term capital gains. In an IRA, that income compounds tax-deferred (traditional) or potentially tax-free (Roth).

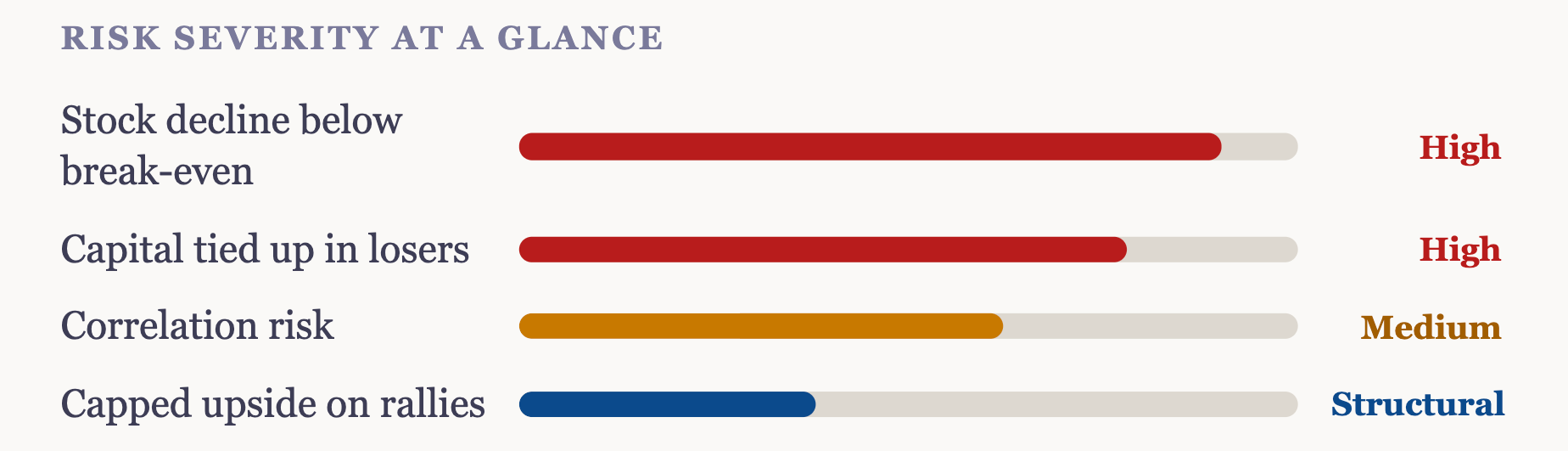

8. What are the actual risks? What can go wrong?

Conservative doesn't mean risk-free.

Here are the real risks, stated plainly.

Stock decline below your break-even.

If a stock drops 15–20% after you sell a put, premium cushions the fall but doesn’t fully protect you. This is why stock selection matters — you run the Wheel on fundamentally sound companies, not the highest-premium names you can find.

Capital tied up in losing positions.

When you’re assigned a stock that’s dropped significantly, your cash is locked in shares. Covered calls at your break-even strike may yield little or nothing. Capital can sit idle for weeks or months. This is why position sizing matters — no single position should exceed 5–10% of your portfolio.

Capped upside on rallies.

Covered calls obligate you to sell at the strike. If the stock rockets past it, you miss the move above. That’s the structural trade-off: consistent premium income in exchange for unlimited upside.

Correlation risk.

If the broad market drops sharply, all your positions can go against you simultaneously. Being assigned on five stocks at once is a real scenario. Sector diversification and a cash reserve are the defense.

None of these risks are hidden. They’re structural features of the strategy, and every one of them is manageable through stock selection, position sizing, and defined rules.

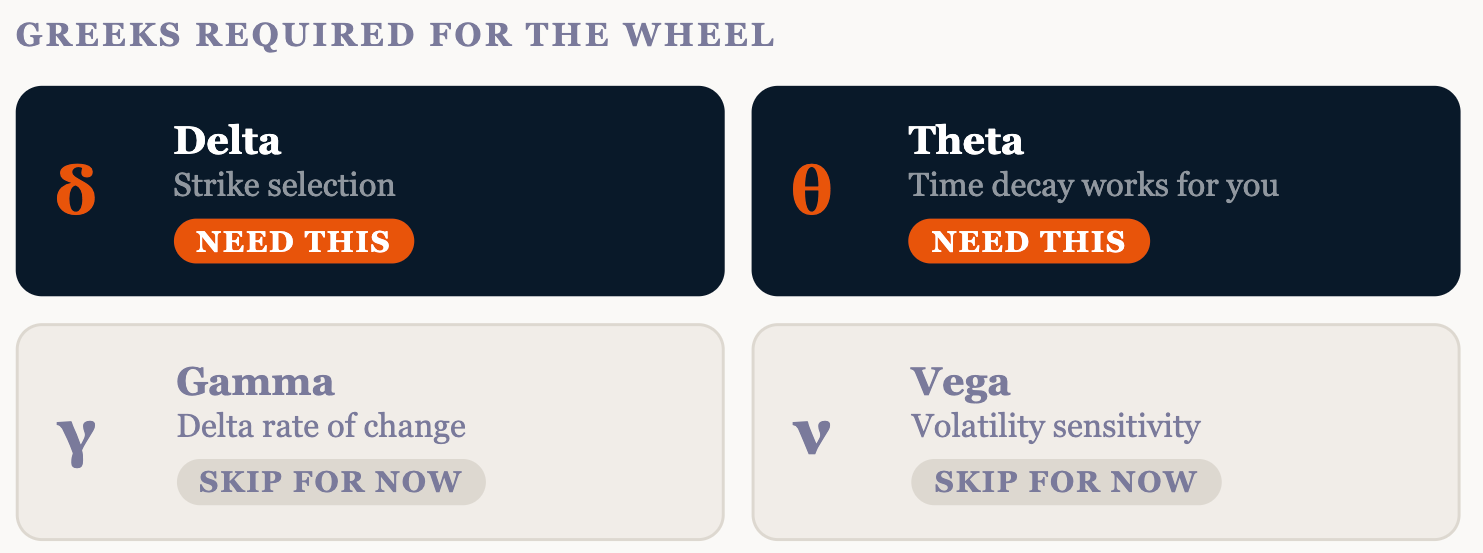

9. Do I need to understand “the Greeks” to run this?

Not all of them. You need two concepts.

Delta approximates the probability your option finishes in-the-money. A delta of 0.25 means roughly a 25% chance of assignment. Most Wheel traders sell puts between 0.20 and 0.35 delta. Your broker displays it right on the option chain — you just pick the number that fits your risk tolerance.

Theta is the rate at which your option loses value each day from time passing. As a seller, this works in your favor. Every day the stock stays above your strike, the option you sold gets cheaper. That’s the core mechanic that makes option selling structurally favorable.

You don’t need gamma, vega, or rho.

You need delta for strike selection and an understanding that time decay is your friend.

For more depth, see:

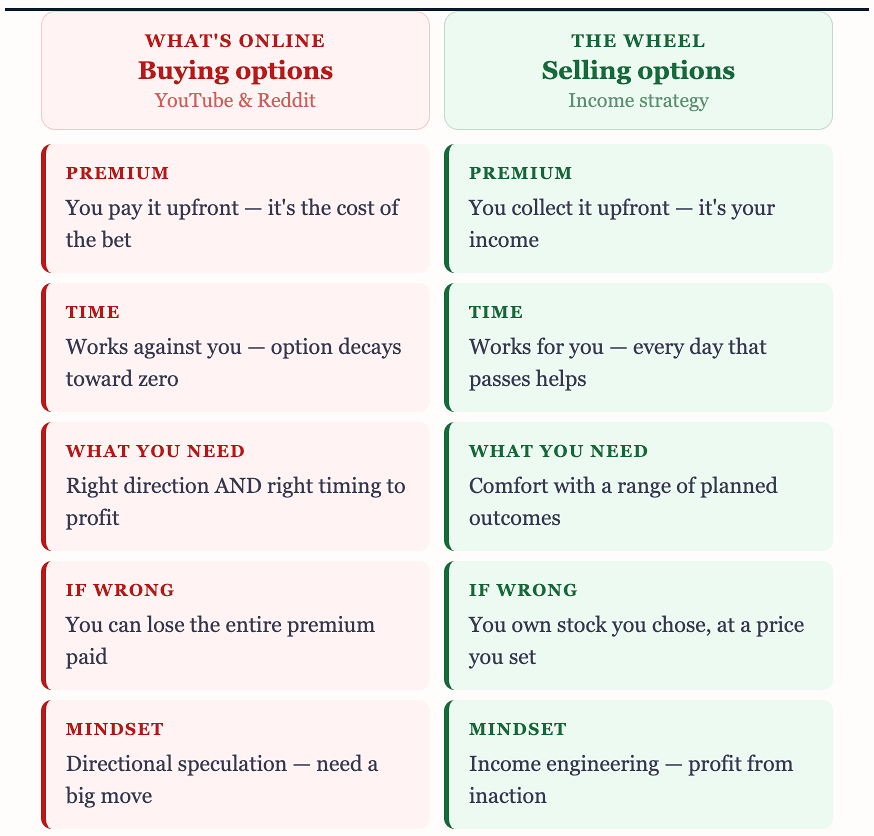

10. How is this different from what I see on YouTube and Reddit?

Most options content online is about buying options — paying premium to bet on direction and timing.

When it works, the gains are big.

When it doesn’t, you lose everything you paid. Time works against you.

The Wheel is the structural opposite.

You sell options and collect premium upfront.

Time works in your favor.

You don’t need to predict direction — you need to be comfortable with a range of outcomes, because you planned for each one in advance.

Option buyers need to be right. Option sellers need to manage risk.

The analogy that fits: buying options is like buying lottery tickets.

Selling options is like being the insurance company — collecting premiums across many transactions, knowing some will cost you, but that over time the math is favorable.

This publication teaches that process.

How to select stocks, choose strikes, manage positions, and handle situations when things don’t go as planned.

Every Monday, subscribers receive a full set of Wheel setups with management plans — because seeing the process applied consistently is how you learn to run it yourself.

This publication exists to teach the Wheel Strategy clearly and help you run it with confidence.