How Option Pricing Works: Premium, Delta, Volatility, and Time

Most people who sell options believe they are trading stocks.

They talk about direction.

They worry about entries.

But option sellers are not paid for being right about price.

They are paid for taking the other side of uncertainty.

Until that mental model is clear, option income feels inconsistent.

Some months look great. Other months feel confusing.

The same setup seems to “work” one week and fail the next.

That randomness is usually an illusion.

The problem is not the strategy.

It’s not the stock. It’s not even bad luck.

It’s misunderstanding what actually creates income.

In this article we break that down in practical terms.

So that when you place a trade, you know exactly why the premium is what it is and what levers you are pulling.

The First Mental Shift - You Are Not Trading Direction

Before we talk about delta, IV, or expirations, one assumption has to die.

You are not paid for guessing where the stock goes.

If direction were the primary driver of income, option sellers would need to outperform analysts, institutions, and algorithms. That’s not realistic. And it’s not required.

When you sell an option, you are entering a contract with very specific terms:

You agree to take action at a predefined price.

You agree to keep capital reserved.

You agree to accept uncertainty until expiration.

The market compensates you upfront for that agreement.

That payment is the premium.

Once you internalize this, the Wheel stops feeling like trading and starts feeling like pricing work. You are evaluating whether the payment offered is sufficient for the obligation you are accepting.

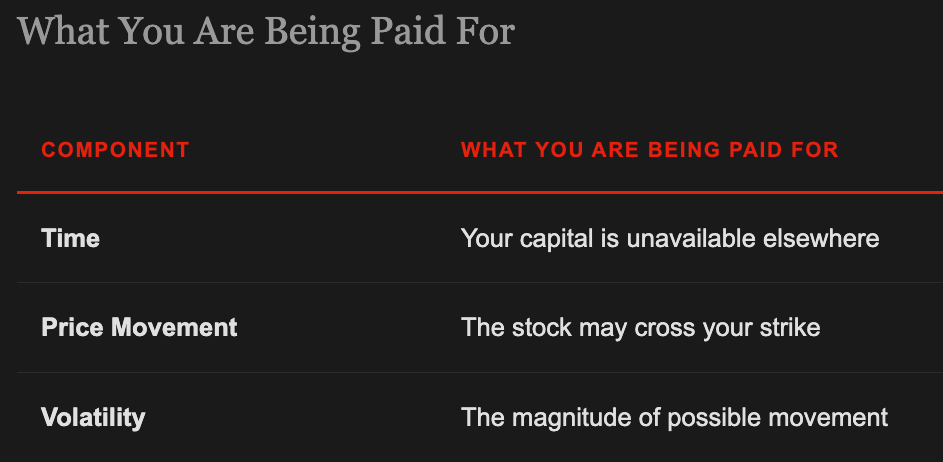

Premium Is the Product - Everything Else Is Secondary

Premium is the entire reason the trade exists.

When you sell a cash-secured put or a covered call, the trade is already profitable at entry. The question is not “will this work?”

The question is “what must happen for me to lose?”

That framing matters.

Premium compensates you for three very specific things.

Nothing else affects option pricing in a meaningful way.

Charts don’t.

Opinions don’t.

News only matters insofar as it affects volatility.

If you ever feel confused about a trade, come back to this table.

Ask which of these three you are being paid for and whether the payment is sufficient.

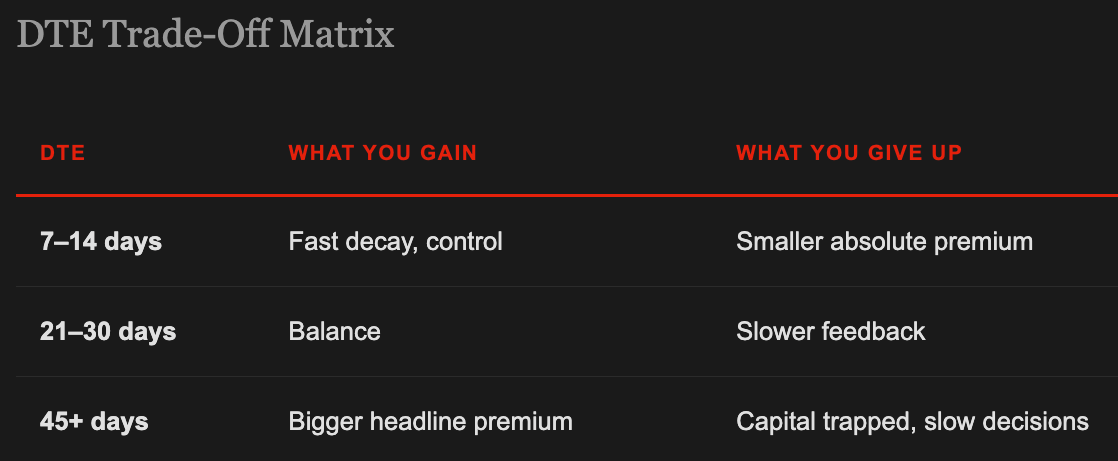

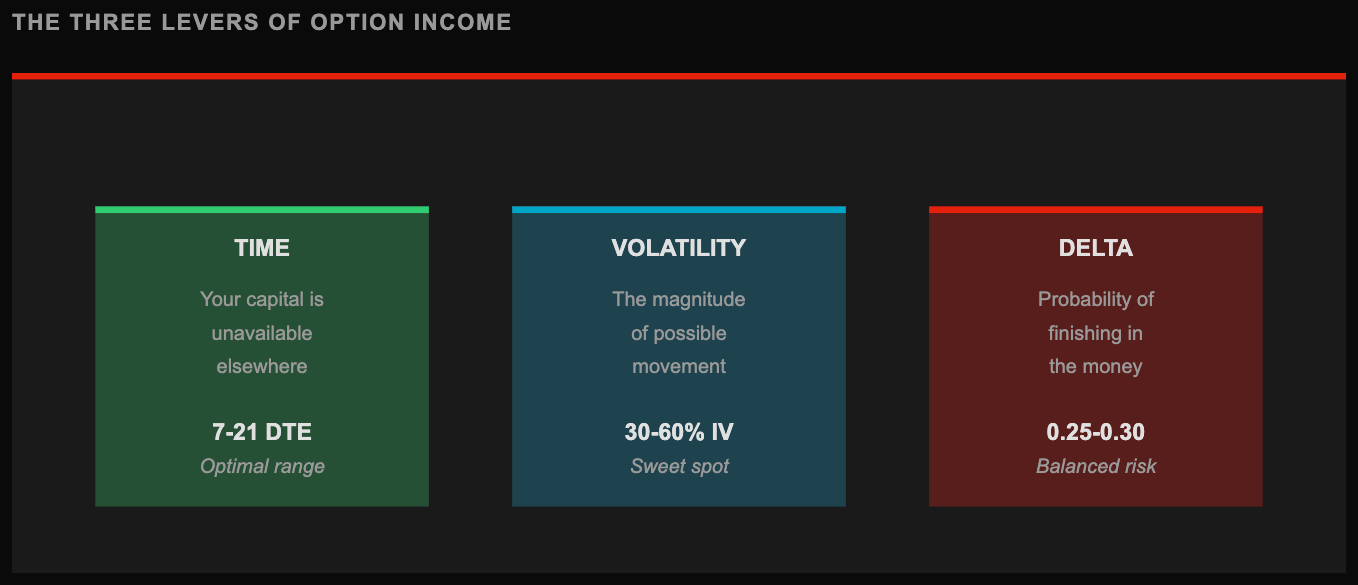

Time - Why DTE Is a Risk Decision, Not a Convenience Setting

Time is the easiest variable to misunderstand.

Longer expirations pay more premium. That is obvious. What is less obvious is what you give up in exchange.

Time does two things simultaneously:

It increases uncertainty.

It reduces flexibility.

A 45-day option looks attractive on paper.

The premium is larger.

The return percentage may even look fine.

But you’ve made a trade-off. You’ve committed capital for six weeks.

If conditions change, your ability to respond is limited.

Adjustments become slower and more complex.

Shorter-dated trades behave differently.

You get paid less per trade, but you get paid more often.

More importantly, you regain control quickly.

This is why many disciplined Wheel traders operate inside 7–21 DTE.

You see results faster. You correct mistakes faster. You don’t sit in uncertainty for months.

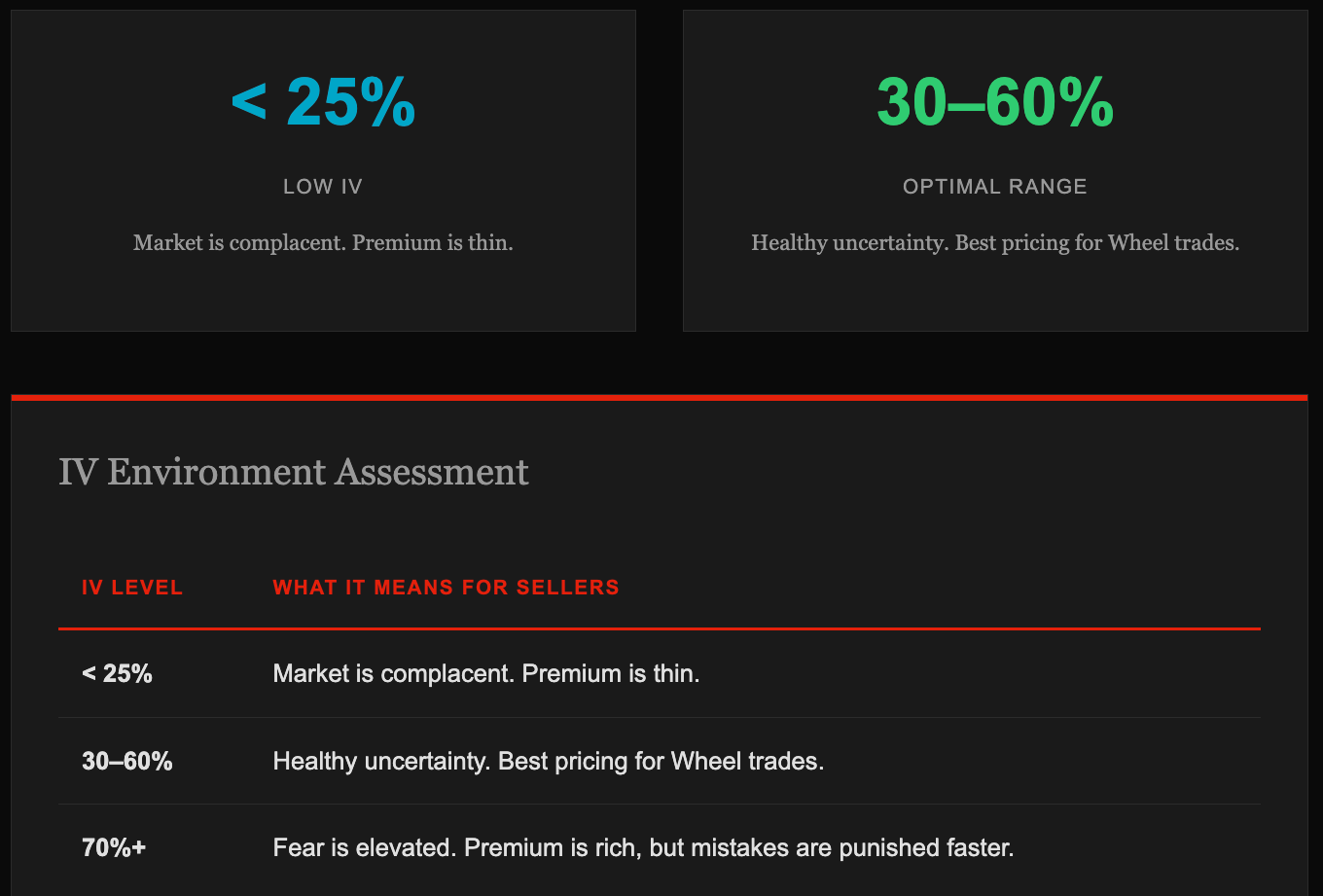

Volatility - Why Fear Is Literally What Pays You

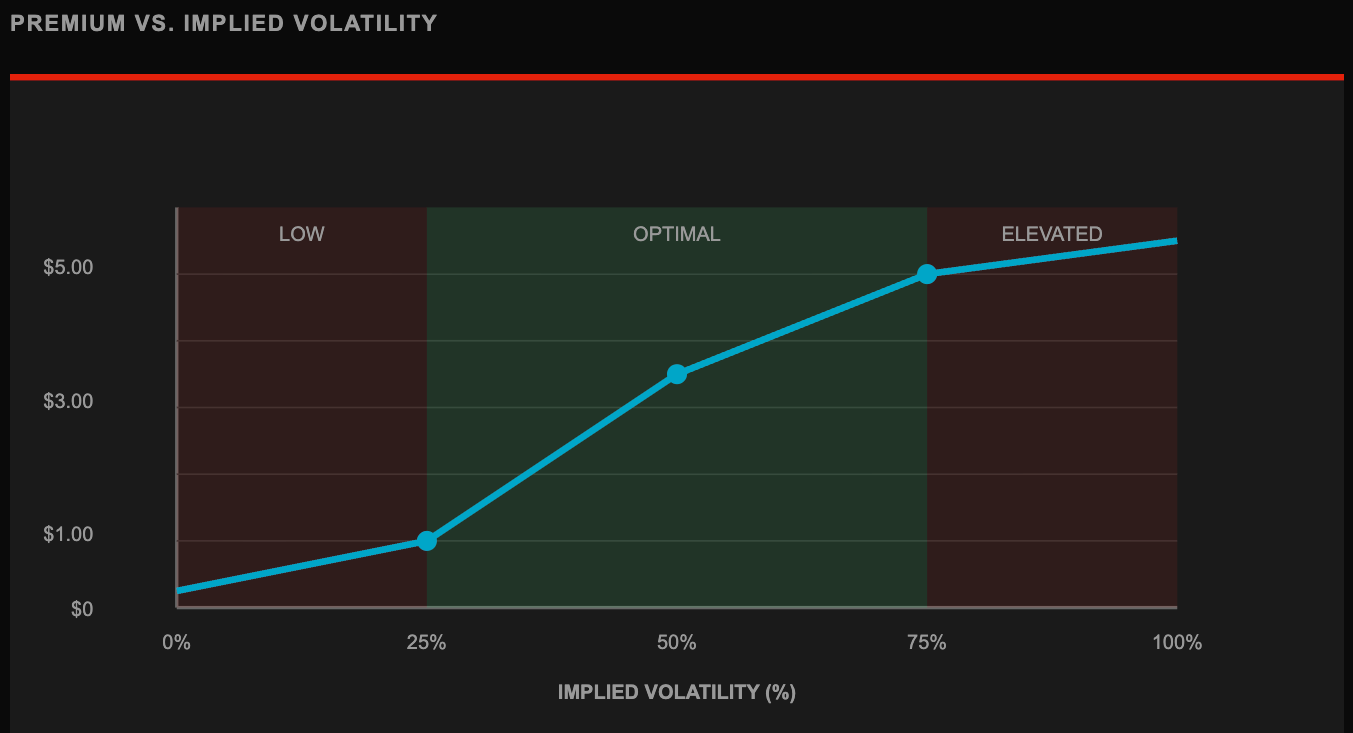

Volatility is often described as “risk.” That’s incomplete.

Volatility is priced uncertainty.

When IV rises, the market is saying one thing clearly:

“We don’t agree on what happens next.”

That disagreement has value.

High IV does not automatically mean “good trade.”

It means you are being offered more money to absorb risk.

Your job is not to chase IV.

Your job is to decide whether the compensation matches the responsibility.

This is why selling options in low-volatility markets feels frustrating.

You’re still taking obligation, but the market isn’t paying you much for it.

And it’s why selling options into moderate fear often feels easier.

The same obligation pays more.

Volatility is not something to predict. It is something to price.

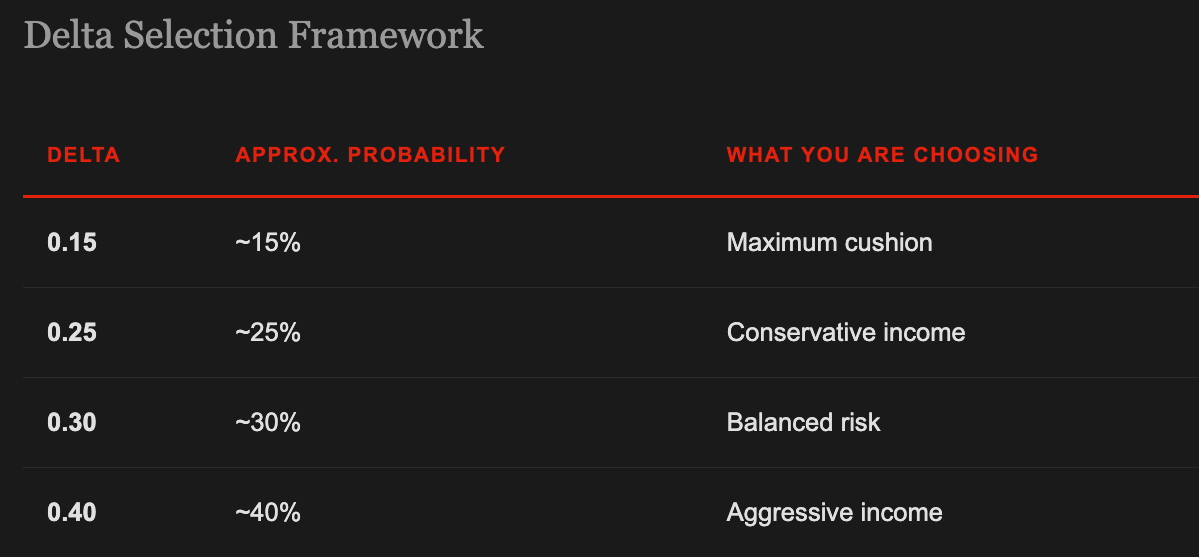

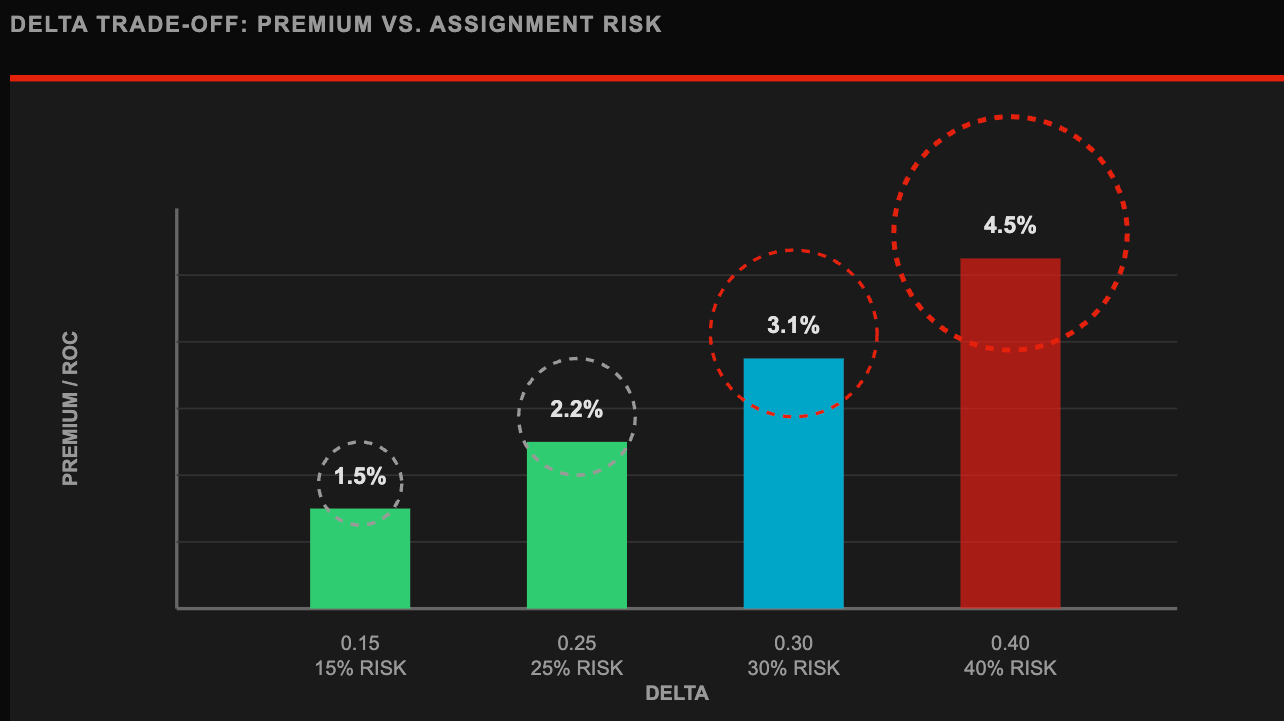

Delta - The Probability Dial You Must Choose Deliberately

Delta is often taught as a technical metric. That obscures its real purpose.

For option sellers, delta is simply a probability estimate.

If a short put has a delta of 0.30, the market is estimating roughly a 30% chance that the option finishes in the money.

That’s all it is.

Higher delta does not mean better.

Lower delta does not mean smarter.

It means you are choosing how often you are willing to be wrong.

Most problems arise when traders don’t consciously choose this.

They drift upward in delta because the premium “looks better,” without acknowledging the increased assignment frequency.

Delta should be selected before premium. Not after.

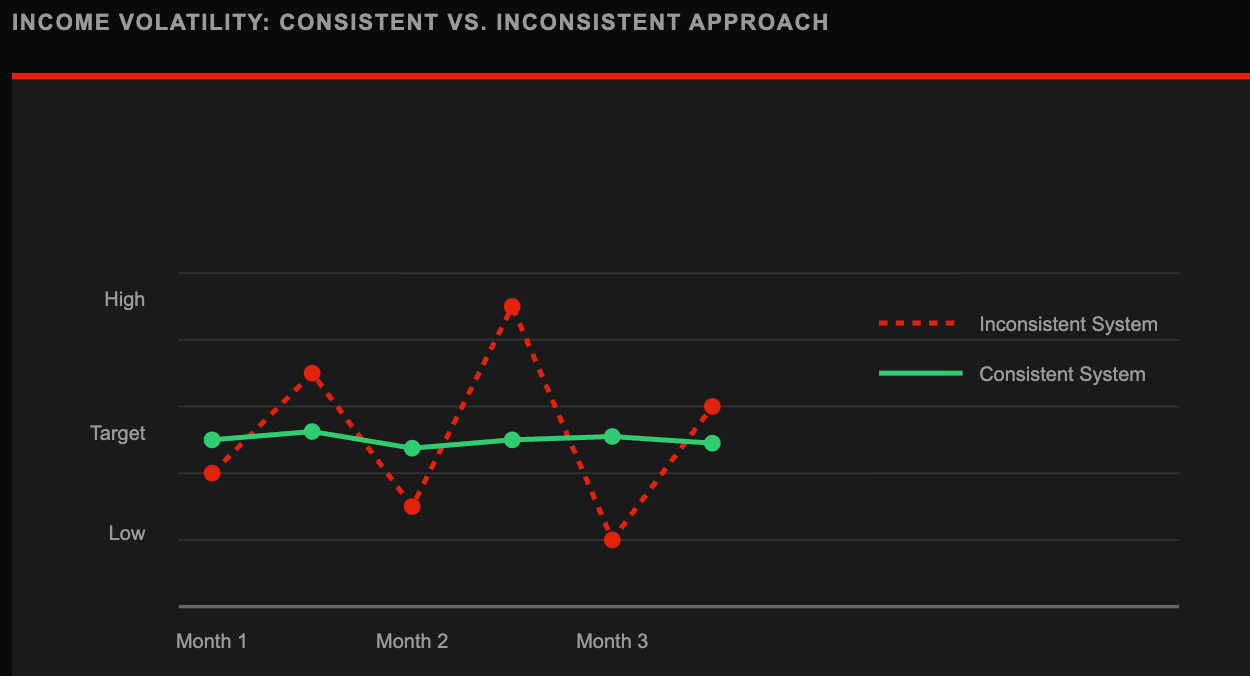

Why Income Feels Random When the Mechanics Are Ignored

Many traders describe Wheel income as “uneven.”

One month looks clean.

Next month feels heavy.

Nothing obvious changed, yet results did.

This usually happens when trades are evaluated one by one, instead of as a pricing system.

Option income is not smooth by default.

It becomes smooth when probability, sizing, and time are aligned.

Randomness creeps in when:

Delta varies trade to trade without intent

DTE jumps around based on convenience

Position size adapts to confidence instead of rules

At that point, outcomes depend on luck sequencing. Not on structure.

The Wheel is not designed to avoid losses.

It’s designed to make outcomes survivable and repeatable.

That only works when pricing decisions are consistent.

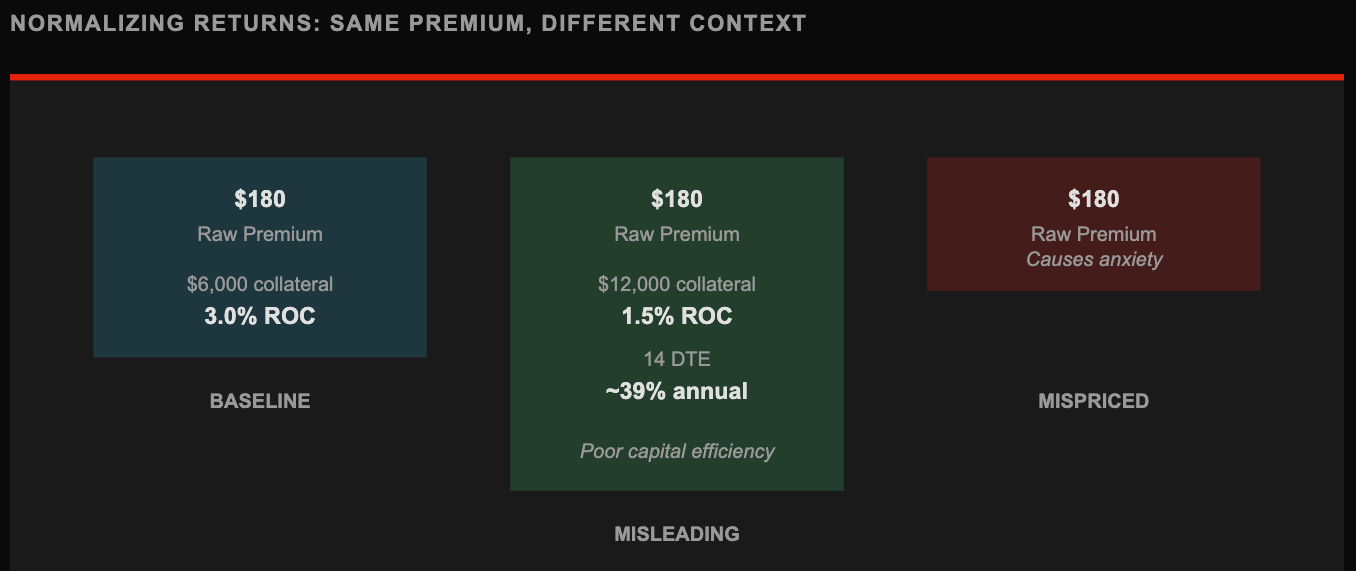

Normalizing Premium - The Only Way to Compare Trades Properly

Raw premium numbers are meaningless.

“$180 collected” tells you nothing without context.

You must normalize every trade the same way, or you will misjudge risk and performance.

There are three normalizations that matter.

1. Premium Relative to Collateral

This answers one question:

How hard is my capital working?

Example:

Premium: $120

Strike: $4,000 collateral

Return = 3.0%

This tells you what the trade earns if nothing goes wrong.

Always calculate this first.

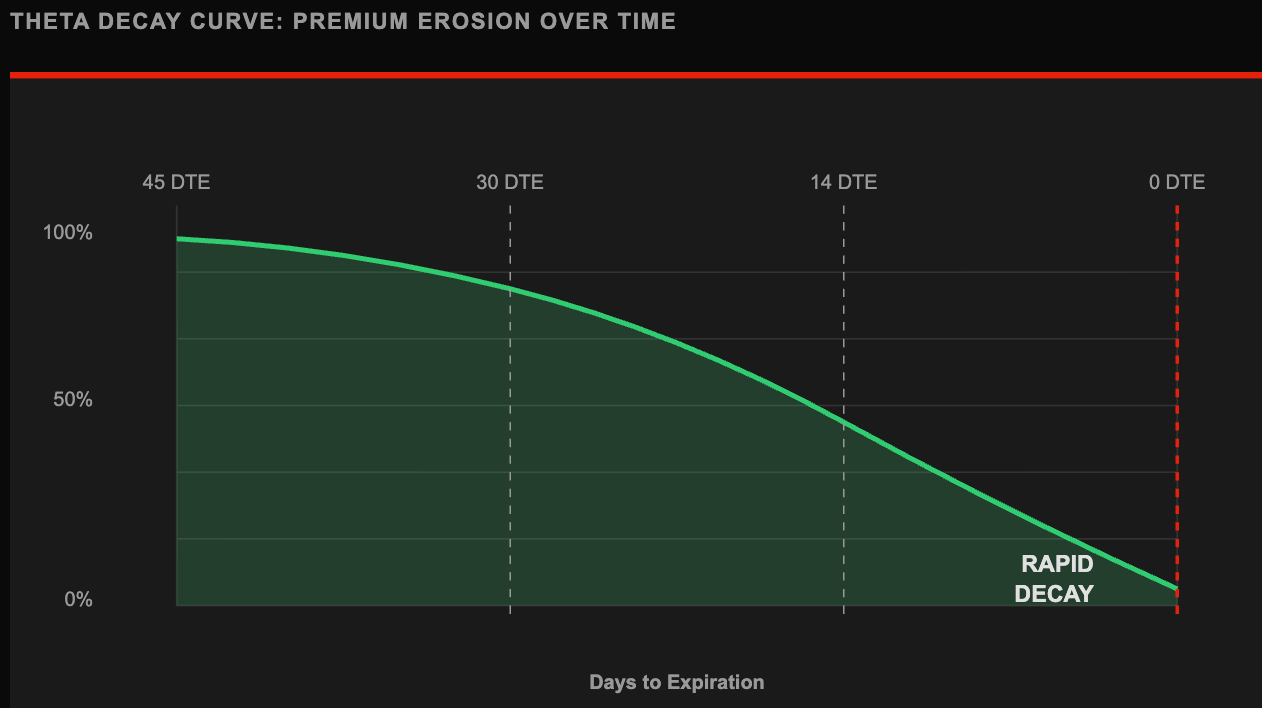

2. Premium Relative to Time

This tells you whether capital is being used efficiently.

3.0% over 14 DTE

≈ 6.4% per month (not compounded)

This does not mean you will earn that monthly.

It tells you how fast the trade works when it works.

Fast decay gives feedback. Slow decay hides mistakes.

3. Premium Relative to Stress

This one is subjective but critical.

Ask:

Will I watch this position every hour?

Will a 5% stock drop make me anxious?

Will assignment force a decision I’m not ready for?

If yes, the premium is not sufficient. No matter how good the math looks.

Premium that disturbs behavior is overpriced.

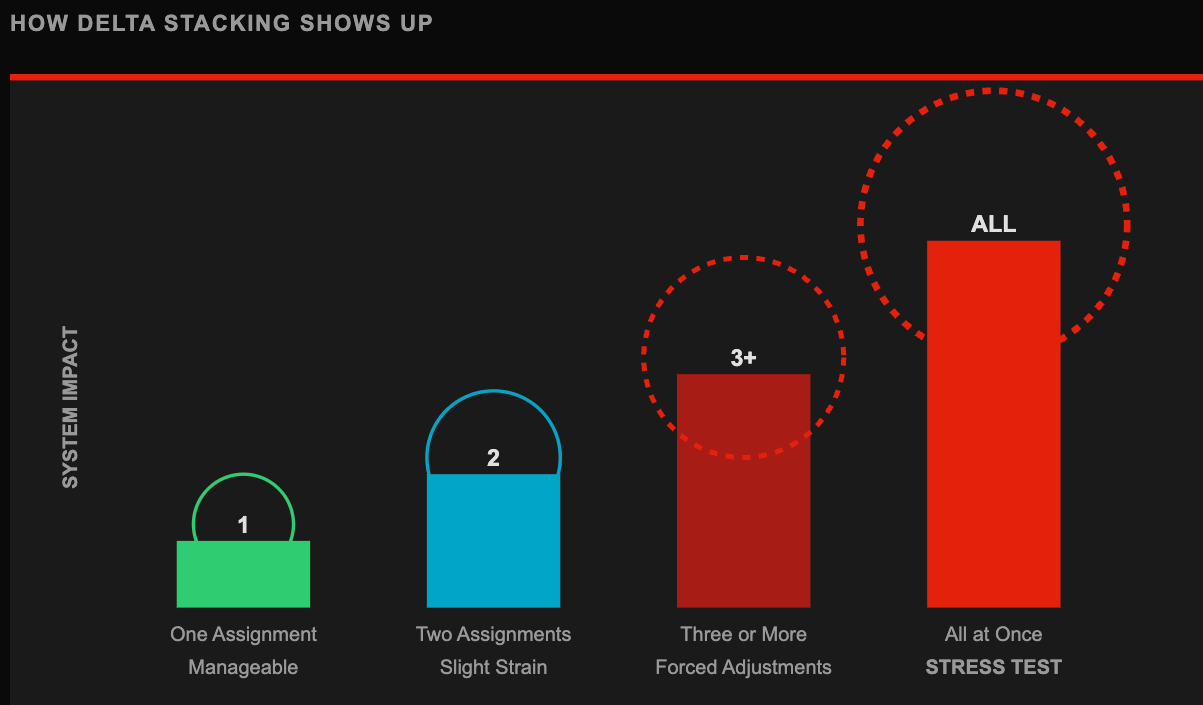

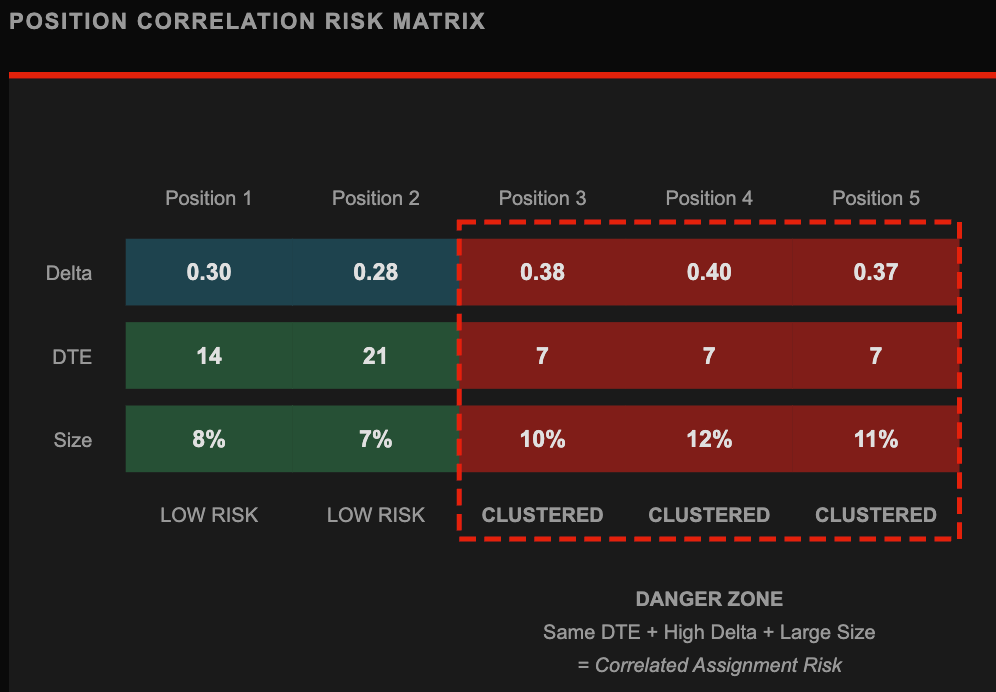

Delta Stacking - The Hidden Source of Blowups

One high-delta trade rarely causes problems.

Multiple high-delta trades expiring together often do.

This is called delta stacking, even if traders don’t name it.

Here’s what it looks like in practice:

Five short puts

All 0.35–0.40 delta

Same expiration week

Same market environment

If the market pulls back even modestly, several positions move ITM at once.

Assignment itself isn’t the problem.

Forced decisions under pressure are.

How delta stacking shows up

ScenarioResultOne assignmentManageableTwo assignmentsSlight strainThree or moreForced adjustmentsAll at onceStrategy stress test

This is why income can feel fine for weeks, then suddenly chaotic.

Nothing “broke.” Probabilities simply resolved together.

How to control it

Vary delta across positions

Stagger expirations

Limit total capital exposed to similar strikes

Delta is not dangerous alone. Correlation is.

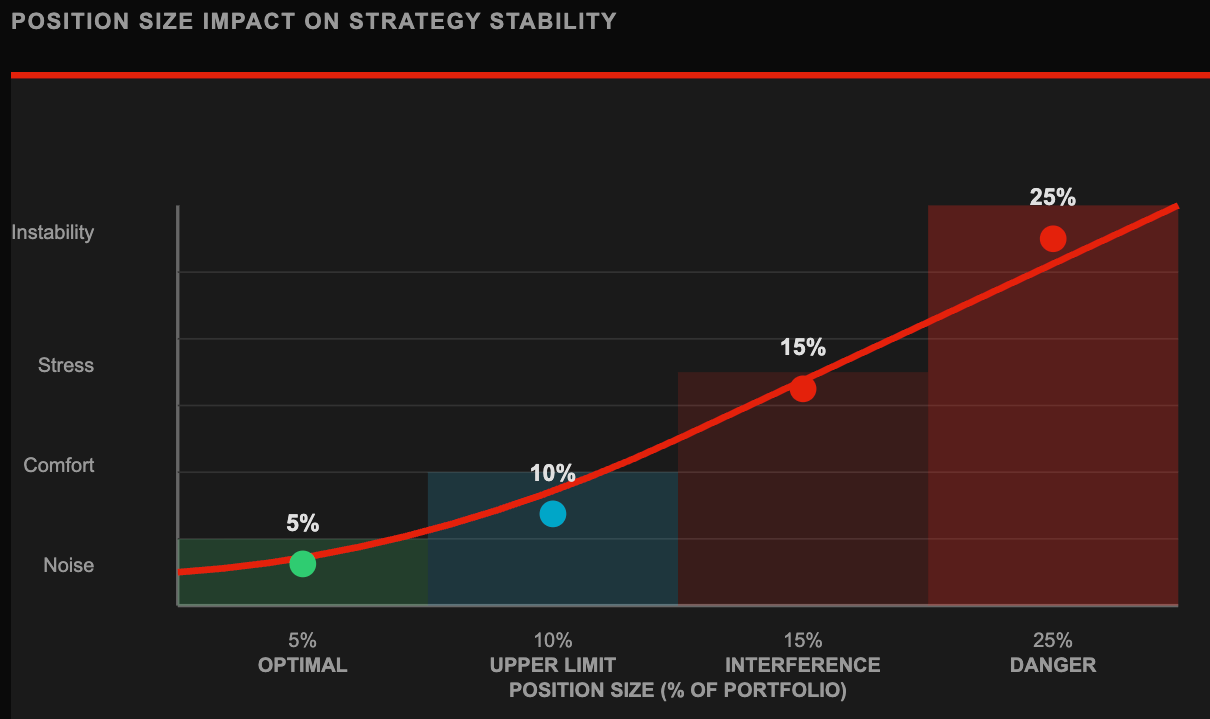

Position Size - The Only Rule That Overrides Everything Else

You can survive:

Poor timing

Lower IV

Slightly aggressive delta

You cannot survive poor sizing.

Position size determines whether a mistake is a lesson or a wound.

Oversized positions remove optionality.

They force holds, force rolls, force hope.

Proper sizing restores choice.

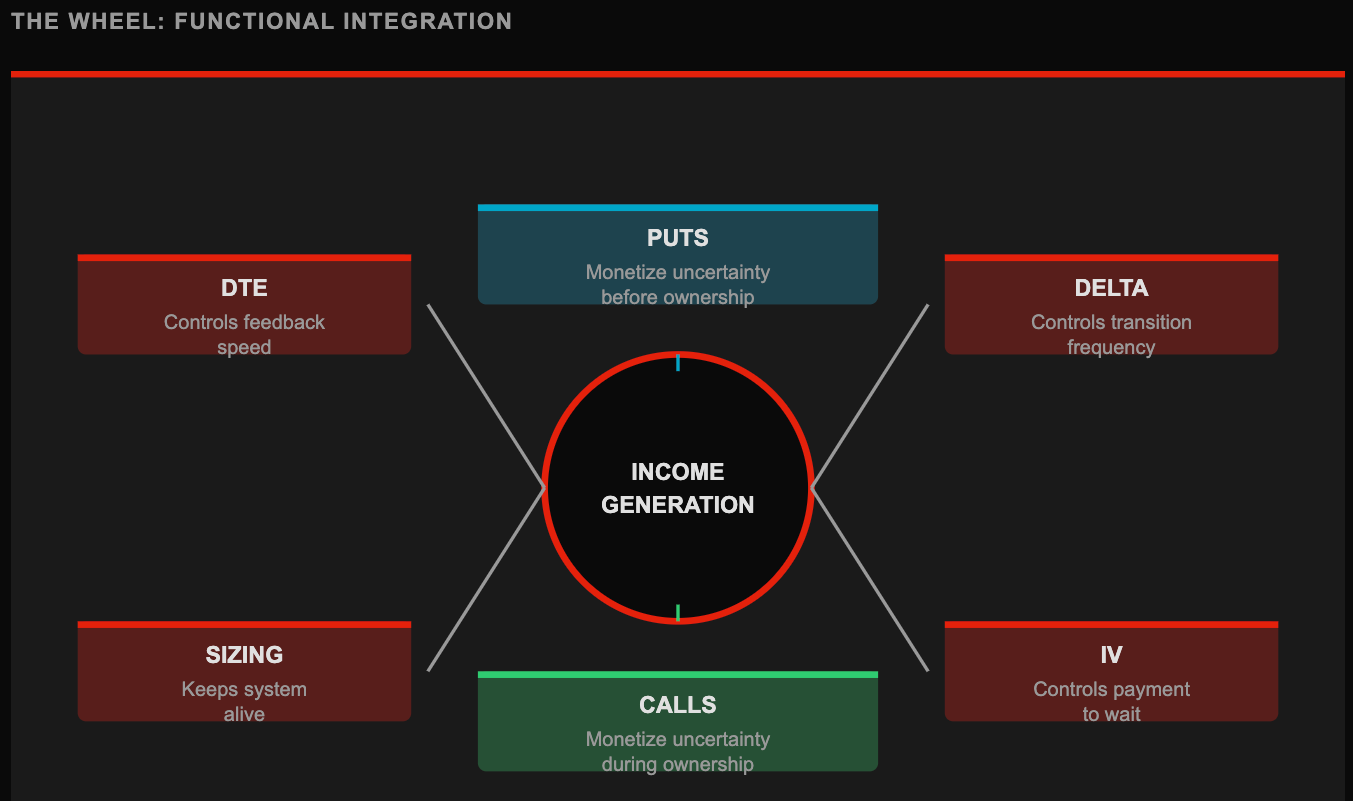

How This All Integrates Into the Wheel

The Wheel is often described as “sell puts, get assigned, sell calls.”

That’s mechanically correct.

But mechanically correct descriptions hide why it works.

Here’s the functional view:

Puts monetize uncertainty before ownership

Calls monetize uncertainty during ownership

Delta controls frequency of transitions

IV controls how much you’re paid to wait

DTE controls feedback speed

Sizing keeps the system alive

Assignment is not a failure state.

It is a state change.

Income continues on both sides as long as pricing discipline stays intact.

A Concrete Pre-Trade Calibration Framework

Before placing any trade, walk through this in order.

On paper if needed.

At this strike, would I want to own the stock?

What delta am I choosing, and why?

Is IV compensating me adequately?

What percentage of my portfolio does this consume?

If assigned tomorrow, would my plan be clear?

If any answer is vague, the trade is premature.

Clarity before entry prevents emotional management later.

Once these mechanics are internalized, something shifts.

You stop reacting to price.

You stop chasing premium.

You stop forcing trades.

Premium is evaluated, not desired.

Delta is chosen, not drifted into.

Time is controlled, not endured.

That’s when the Wheel stops feeling risky, because it becomes priced, bounded, and intentional.