Running the Wheel Strategy Inside a Roth IRA: Everything You Need to Know

Running the Wheel Strategy inside a Roth IRA means every dollar of premium collected — every expired put, every covered call, every assignment cycle — compounds tax-free.

For a strategy built on repeated short-term premium, that changes the math in a way worth understanding before opening a single position.

Can You Actually Sell Puts in an IRA?

Yes.

Every major U.S. broker allows cash-secured puts and covered calls inside both Roth and Traditional IRAs. Schwab, Fidelity, Interactive Brokers, Tastytrade, E*TRADE, Robinhood, Webull — all of them.

The approval you need varies by broker, but the bar is low.

At Schwab, cash-secured puts fall under Level 0, the most basic options tier. At Fidelity, you need Level 2. At Robinhood Retirement, Level 2 covers it.

The application takes five minutes and asks about your trading experience, income, and risk tolerance. Most approvals come back the same day.

What you cannot do in an IRA is anything that requires borrowing. No naked calls. No naked puts beyond your available cash. No short selling. No margin. The IRS prohibits IRAs from taking on debt, which means every put you sell must be fully backed by cash already sitting in the account.

That restriction sounds limiting, but it lines up perfectly with the Wheel. Cash-secured puts are already the entry point. Covered calls require owning the shares. Neither leg of the strategy needs margin to function.

Why Does the Roth Beat a Traditional IRA for Premium Sellers?

Both Roth and Traditional IRAs shelter your trades from annual taxes while the money stays inside the account.

The difference shows up when you take the money out.

Traditional IRA:

Every dollar withdrawn gets taxed as ordinary income at your marginal rate. It does not matter whether the gains came from stock appreciation, dividends, or options premium. There is no long-term capital gains treatment. A $50,000 withdrawal in retirement adds $50,000 to your taxable income for the year.

Roth IRA:

Withdrawals are tax-free, permanently — as long as the account has been open for at least five tax years and you are 59½ or older. Premium collected from selling puts and calls inside a Roth is never taxed. Not when you collect it. Not when you withdraw it.

Taxable account:

Options premium from expired or closed-early positions is taxed as short-term capital gains. For someone in the 32% bracket with the 3.8% net investment income tax and state taxes, that can mean losing 40%+ of every premium dollar to taxes. The same premium inside a Roth loses 0%.

There is one more difference.

Traditional IRAs force you to start taking Required Minimum Distributions at age 73 (75 if born in 1960 or later). Roth IRAs have no lifetime RMDs for the original owner. The money can sit and compound for as long as you want.

For a strategy that generates frequent short-term income — exactly what the Wheel does — the Roth is the strongest available tax wrapper.

If you haven’t subscribed yet — enter your email below to get the weekly setups and educational guides delivered to your inbox.

It’s free, and you can explore the full archive from there.

What Changes When You Run the Wheel Inside a Roth?

The mechanics of the Wheel itself do not change. Sell a cash-secured put, collect premium, wait. If assigned, sell a covered call. Repeat. The cycle works the same inside a Roth as it does in a taxable account.

What changes is the plumbing around it.

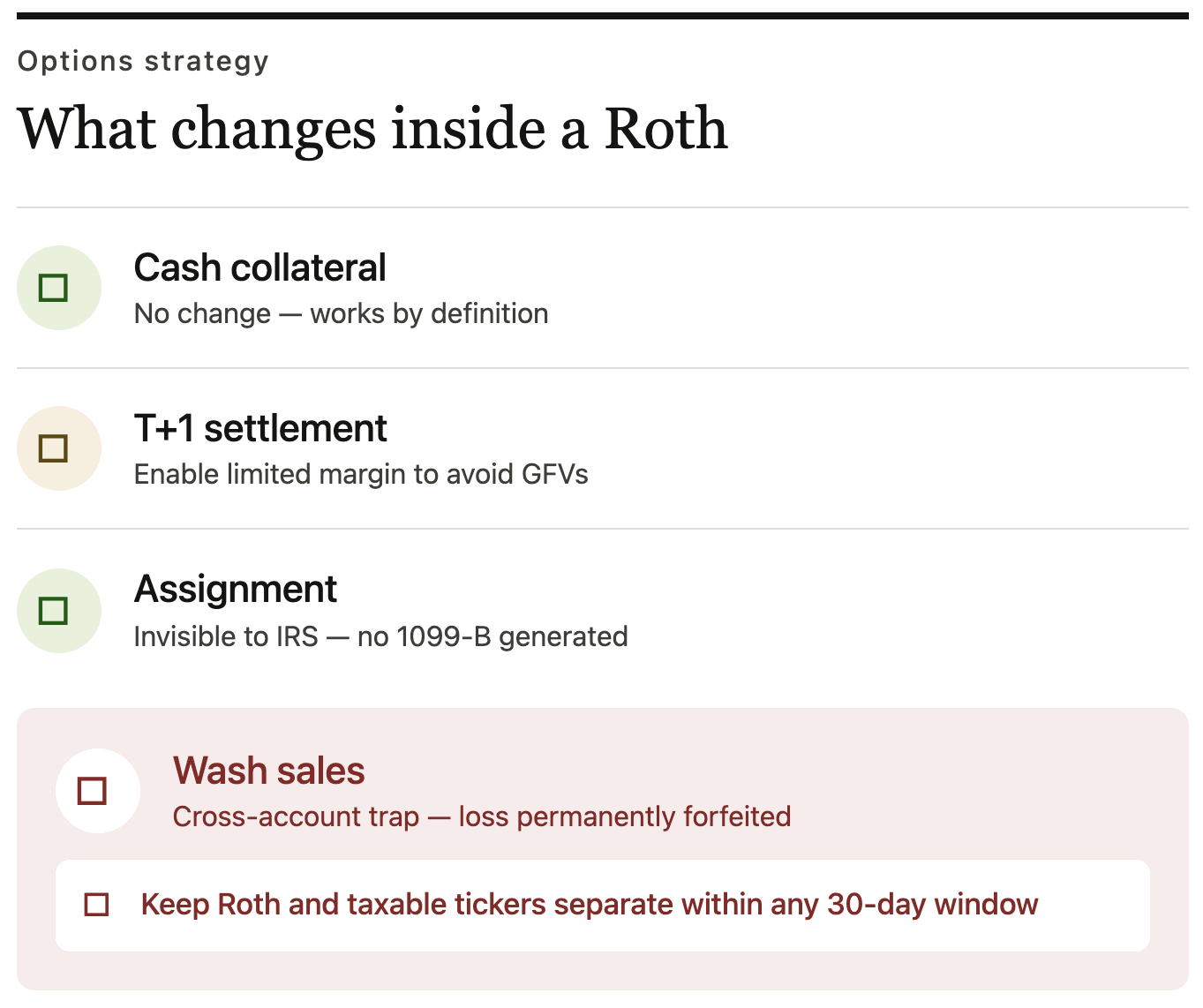

1. Does the Wheel need margin?

A Roth IRA is a cash account. To sell a $50-strike put, you need $5,000 in cash sitting in the account. That cash gets locked as collateral until the put expires or gets assigned. This is exactly how cash-secured puts work by definition, so the constraint is invisible for Wheel traders.

2. How does settlement work in a Roth IRA?

In a pure-cash IRA, proceeds from selling stock or closing an option settle the next business day (T+1). Trading with unsettled funds can trigger a Good Faith Violation. Three of those in 12 months, and some brokers restrict you to settled-cash-only trading for 90 days.

The fix: most brokers offer “limited margin” on IRAs, which sounds like borrowing but is not. It just lets you trade with unsettled proceeds. Schwab, Fidelity, E*TRADE, and Tastytrade all offer it.

3. Does assignment trigger a tax event in a Roth?

When a put gets assigned inside a Roth, cash converts to shares automatically. When a covered call gets assigned, shares convert to cash. No 1099-B is generated. No tax event is reported. The Wheel cycle just continues.

4. Do wash sale rules apply to a Roth IRA?

This is the trap most people miss. Inside the Roth itself, wash sales are irrelevant because losses inside the account never generate tax deductions anyway. But if you sell the same stock at a loss in a taxable account and then get assigned that stock inside your Roth within 30 days, the IRS disallows the loss in your taxable account.

Worse, the disallowed loss does not get added to your Roth’s cost basis. It is permanently gone. Not deferred. Forfeited.

The practical rule: if you wheel a ticker in your Roth, do not sell the same ticker at a loss in your taxable account within a 30-day window. Keep the tickers separate across accounts, and the problem disappears.

Share this guide with another Wheel practitioner you know.

They’ll thank you.

How Do You Size Wheel Positions in a Roth IRA?

Roth IRA contribution limits are $7,500 per year in 2026 ($8,600 if you are 50 or older). That is the cap on new money going in. It means most Roth balances grow slowly unless they are funded by rollovers — converting a Traditional IRA, rolling over a Roth 401(k) at job change, or using a backdoor or mega-backdoor Roth strategy.

The median IRA balance in the U.S. is around $38,000. That is enough for one or two Wheel positions on lower-priced stocks.

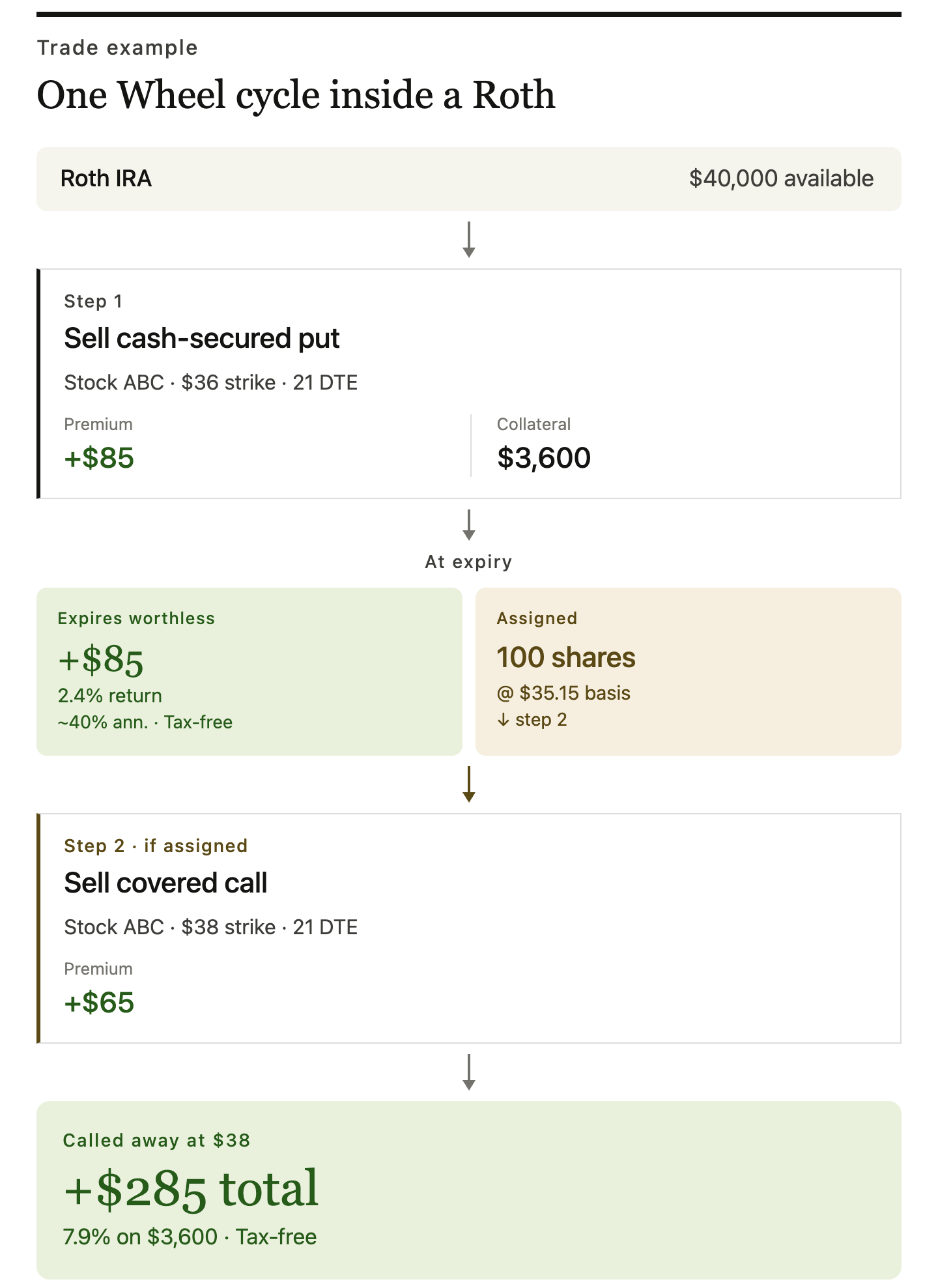

Here is what a Wheel cycle looks like inside a $40,000 Roth.

The put:

Sell one cash-secured put on a $38 stock — call it Stock ABC — at the $36 strike, 21 DTE, for $0.85 credit.

Collateral required: $3,600.

Premium collected: $85.

If the stock stays above $36, the put expires worthless. $85 earned in three weeks on $3,600 of capital. That is 2.4% for the cycle, roughly 40% annualized. All tax-free.

If assigned:

→ 100 shares of Stock ABC land in the account at a cost basis of $35.15 ($36 strike minus $0.85 premium).

→ Sell a covered call at the $38 strike, 21 DTE, for $0.65. Collect another $65.

→ If the stock gets called away at $38, the total gain on the cycle is $285 on $3,600 deployed — premium from both legs plus the $2.85 per share gain. Tax-free.

On a $40,000 account running two positions at a time, collecting 1–2% per cycle across 12–15 cycles per year, the account generates roughly $4,000–$8,000 in annual premium income. In a taxable account at a 35% combined tax rate, that is $2,600–$5,200 after tax. In a Roth, it is $4,000–$8,000. The spread grows every year as the account compounds.

A $100,000 Roth — achievable through conversions and rollovers — can run four or five Wheel positions simultaneously with proper diversification. The income scales, and none of it gets touched by the IRS.

Quick Reference

Can you sell cash-secured puts in a Roth IRA?

Yes. Every major U.S. broker allows it with basic options approval (typically Level 1 or Level 2).

Can you sell covered calls in a Roth IRA?

Yes. You need to own 100 shares per contract in the same account.

What is NOT allowed?

Naked calls, naked puts beyond available cash, short selling, margin borrowing.

Is premium income taxed?

No — if withdrawn as a qualified distribution (account open 5+ years, age 59½+).

Are there RMDs?

No. Roth IRAs have no Required Minimum Distributions for the original owner.

What about wash sales?

Inside the Roth, they are irrelevant. But selling the same stock at a loss in a taxable account within 30 days of acquiring it in the Roth permanently forfeits the loss.

Contribution limits (2026)?

$7,500 standard, $8,600 if 50 or older. Income phase-outs apply.

How do most people build a large Roth?

Roth conversions from Traditional IRAs, Roth 401(k) rollovers, and mega-backdoor Roth contributions over multiple years.

The Wheel and the Roth are structurally aligned.

Both already require cash-secured positions. Both reward patience over speculation. The Roth just removes the tax drag that erodes premium income in a taxable account — and for a strategy that generates income through frequent short-term trades, that drag is real.

The compounding advantage of zero-tax premium income shows up slowly. It is most visible a decade from now, in the account that kept every dollar it earned.

Most investors learn the Wheel. Few run it week after week.

The paid tier is the operational system: fifteen full Wheel setups every Monday with management plans for each position, ten pre-filtered cash-secured puts every trading day, and a printable PDF of the weekly report.

Free subscribers see five setups. Paid subscribers see all fifteen.

The full breakdown is on the page below. Pricing is transparent, and the first 30 days are covered by a money-back guarantee.