The 7 Most Common Wheel Strategy Mistakes (and How to Fix Each One)

The Wheel itself is a sound strategy — sell cash-secured puts on quality stocks, take assignment when it comes, sell covered calls until the shares get called away, repeat.

The mechanics are simple.

But the execution has enough traps that beginners tend to find every one of them before they find their rhythm.

This article covers the seven mistakes that show up most often in Wheel trading, why each one costs money, and the specific fix for each.

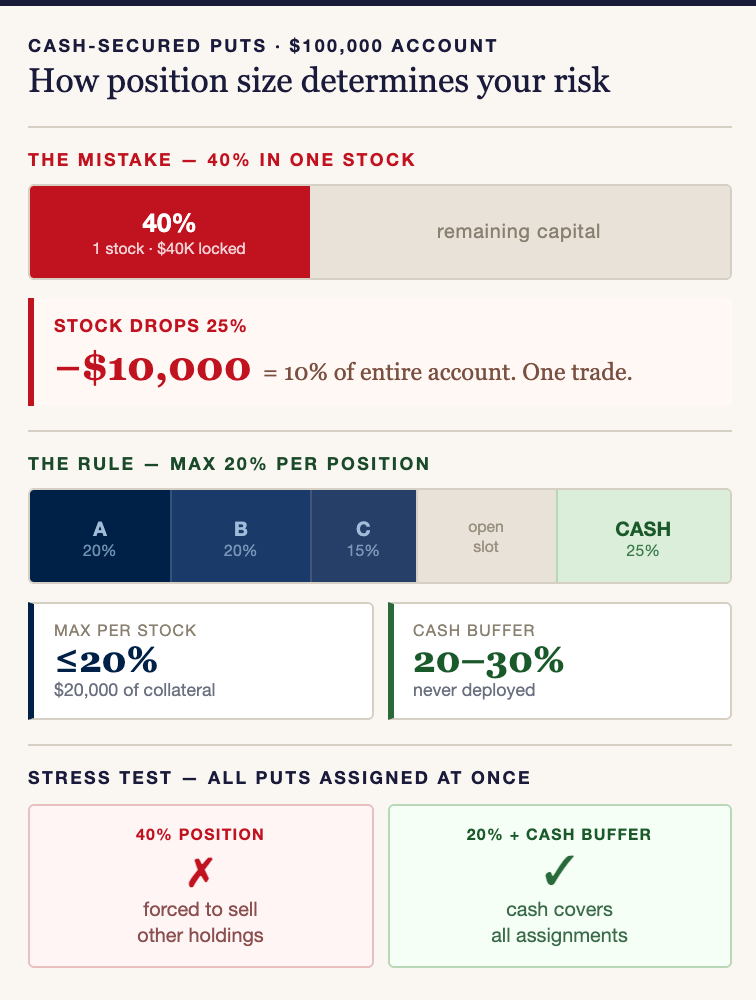

1. Oversizing Positions

When you sell a cash-secured put, you’re setting aside the full amount needed to buy 100 shares if assigned.

That collateral is locked up until the contract expires or you close it.

The mistake beginners make is putting too much of their account into a single stock.

Say you have a $100,000 account and you sell cash-secured puts on one stock that tie up $40,000 in collateral. That’s 40% of your account riding on a single name. If that stock drops 25%, you’ve just lost $10,000 — 10% of your total portfolio — from one position.

Now imagine you did this on two or three stocks at the same time and the whole market sells off. That’s how accounts blow up.

The rule most practitioners converge on: no single position should tie up more than 20% of your account, and you should keep 20-30% of your total capital in cash at all times, undeployed.

Here’s what that looks like on a $100,000 account:

Maximum collateral per stock: $20,000 (20% of account)

Cash reserve: $20,000-$30,000 (never deployed)

Working capital for all positions combined: $70,000-$80,000

That cash reserve exists for one reason: if multiple puts get assigned in the same week — which happens during market selloffs — you don’t get forced into selling other positions to cover.

The fix:

Cap each position at 20% of your account value

Keep 20-30% of total capital in cash as a buffer

Before opening a new trade, ask: what happens if every open put gets assigned at the same time? If the answer is “I can’t cover it,” you’re oversized

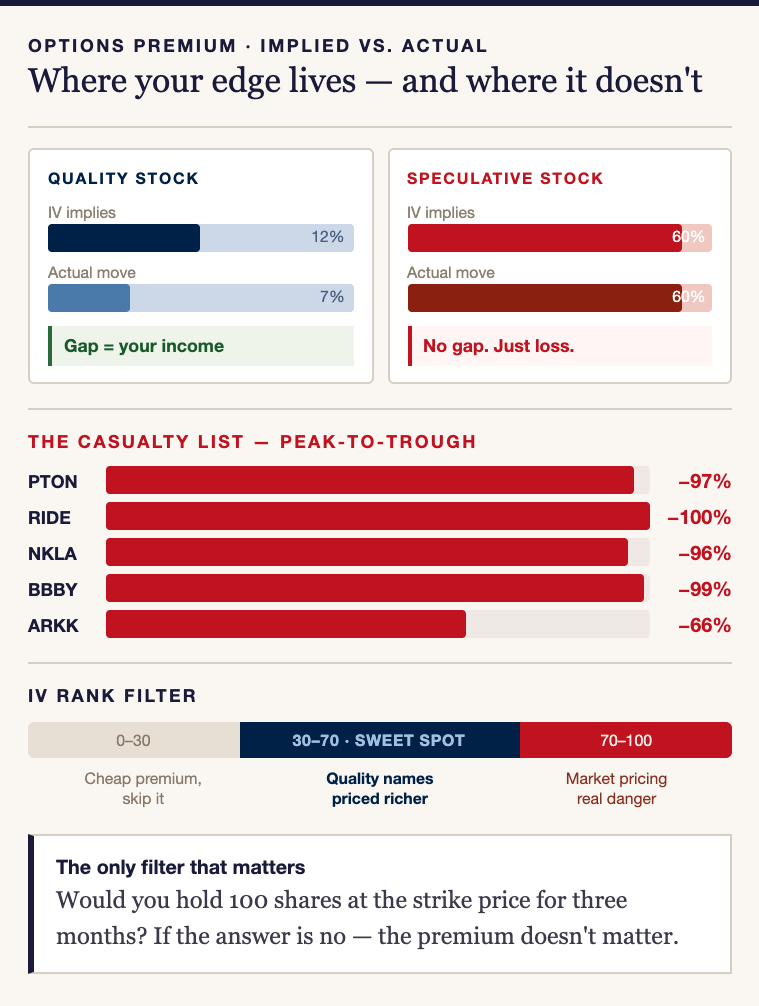

2. Chasing High-IV Junk

A $20 biotech with 150% implied volatility might pay $3.00 in premium on a monthly put. That’s a 15% return in 30 days. It looks like free money — until the stock drops 60% and you’re assigned on shares that may never recover.

The premium is high because the risk is high.

When implied volatility is 150%, the options market is pricing in the real possibility that this stock could halve. That isn’t an opportunity. That’s a warning.

This matters because premium selling works differently on quality stocks than on speculative ones.

On stable, profitable companies, options tend to be priced slightly richer than the moves that actually happen — and that gap between what the market fears and what actually occurs is where Wheel income comes from.

On speculative stocks, the feared move is usually the one that happens. The premium you collect doesn’t cover the loss you take when it does.

The casualty list is long and specific:

RIDE (Lordstown Motors) — went bankrupt

PTON (Peloton) — dropped 97% from its peak

ARKK — lost two-thirds of its value

SPCE, NKLA, BBBY — same pattern

Every one of these offered fat premiums that attracted put sellers who had no business owning the stock at any price.

Meme stocks like GME and AMC are the same trap — they can move 30-50% in a single session on social media momentum alone.

How to screen for this:

Use IV Rank instead of raw IV.

IV Rank measures where a stock’s current volatility sits compared to its own history over the past year. An IV Rank of 60 on a stock like AAPL or JPM means options are priced richer than usual on a stable company — that’s a good time to sell premium. An IV Rank of 60 on a pre-revenue biotech means the market is only moderately scared, and it could get much worse.

But the simplest filter is this: would you buy and hold 100 shares of this stock at this price for the next three months? If the answer is no, the premium doesn’t matter. Don’t sell the put.

The fix:

Only sell puts on stocks you’d own outright at the strike price

Use IV Rank between 30-70 on quality names as your volatility filter

If the annualized premium yield on a setup is above 15%, treat that as a warning sign — the market is telling you something about the risk

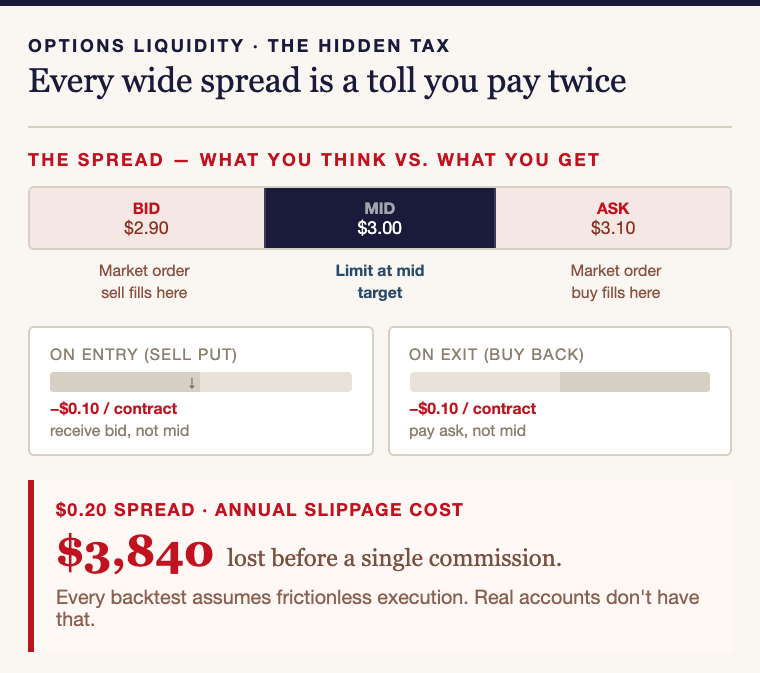

3. Ignoring Liquidity

When you sell a put on a stock with wide bid-ask spreads and thin options volume, you pay a hidden tax on every entry and exit. Option Alpha quantified this: on options with a bid-ask spread of just $0.20, slippage costs alone can exceed $3,840 per year. That’s not commissions — that’s the gap between what you think you’re getting and what you actually receive.

It gets worse under pressure. When you need to close a position during a sudden move, the spread widens. You’re paying the liquidity tax on the way in and double-paying on the way out.

Every options backtest assumes frictionless execution.

Real accounts don’t have that. Bid-ask slippage is the reason backtested returns almost always overstate what you’ll actually collect.

The fix:

Minimum daily options volume: 1,000+ contracts

ATM bid-ask spread: under $0.10

SPY, QQQ, IWM, and most large-cap S&P 500 names clear these thresholds

Always place limit orders at mid — never market orders on options

If you can’t fill within a few cents of mid, the chain is too thin. Move on.

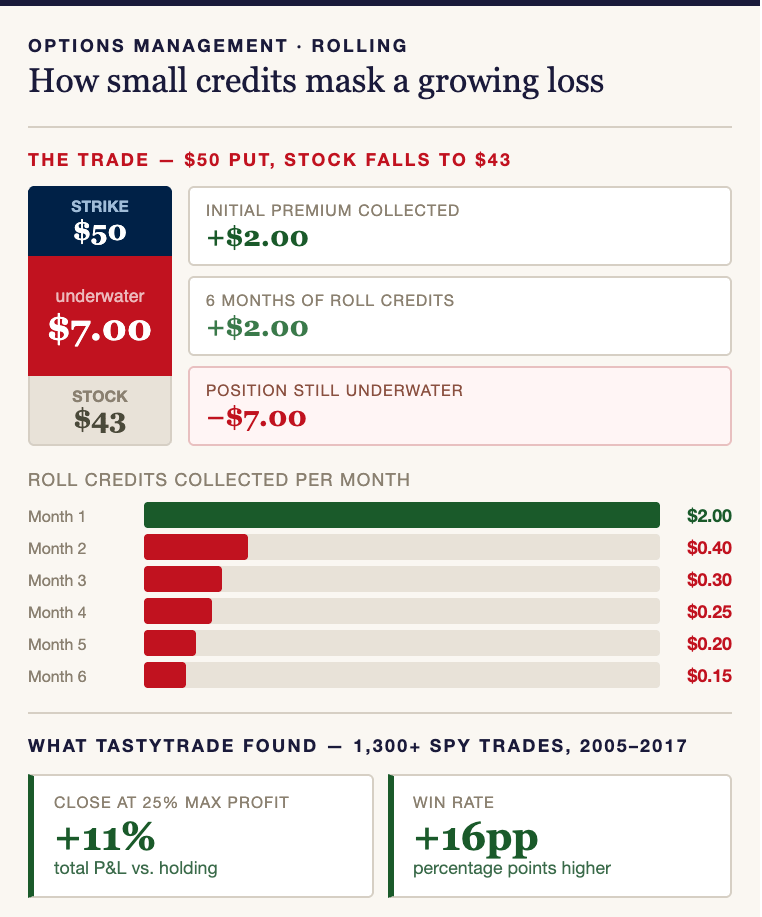

4. Rolling Blindly

Rolling a losing position is sometimes the right move.

Rolling every losing position automatically — because you read that you should always roll for credit — is how small losses become capital traps that last months.

Tastytrade studied over 1,300 SPY strangle trades (2005–2017) and found that closing at 25% of max profit — rather than holding for recovery — increased total P&L by ~11% and win rate by 16 percentage points. Taking profits early and redeploying capital beats sitting in a trade hoping it turns around.

The same trap hits the call side. Traders have kept rolling TSLA covered calls month after month to collect small credits, ending up with shares locked for a full year with capped upside. Each roll felt like a win. The total cost was twelve months of dead capital.

Only roll when all three conditions are met:

You’d open this position fresh today. If you wouldn’t sell this put right now on its own merits, don’t roll into it for another month.

The credit is meaningful. At least half your original premium. A $0.15 credit on a $2.00 position isn’t a reason to stay in.

Your original thesis still holds. Bad earnings, a lost contract, a sector shift — any of these breaks the trade. Close and move on.

Share this article with another Wheel practitioner you know.

They’ll thank you.

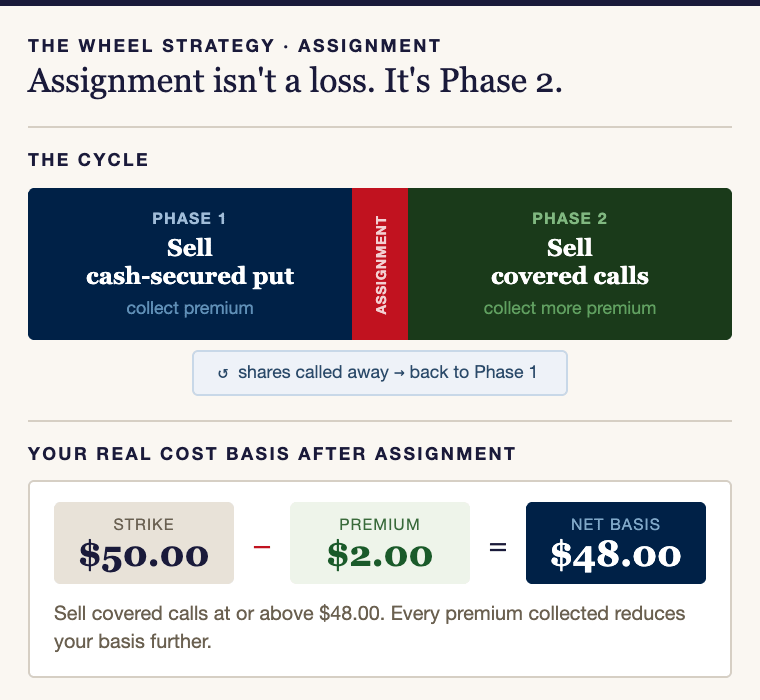

5. Treating Assignment as Failure

Beginners who see assignment as a loss do one of two things: panic-sell the shares, or aggressively sell covered calls below cost basis to “get something back.” Both responses destroy the structural advantage the Wheel is designed to produce.

Assignment is Phase 2 of the cycle.

You own 100 shares at a strike you chose, with a cost basis already reduced by the premium you collected. You sell covered calls against those shares and collect more premium while the stock works its way back. That’s not a loss — that’s the mechanism.

The CBOE PUT Index takes assignment at the ATM strike every month by design and still returned 9.54% annualized over three decades. Assignment isn’t the strategy breaking. It’s the entry point for the next phase.

The fix is simple:

Only sell puts on stocks you’d own at the strike price. This one filter eliminates assignment fear entirely — if you get assigned, you got what you asked for and got paid for it.

When assigned, sell covered calls at or above your net cost basis (strike price minus premium collected).

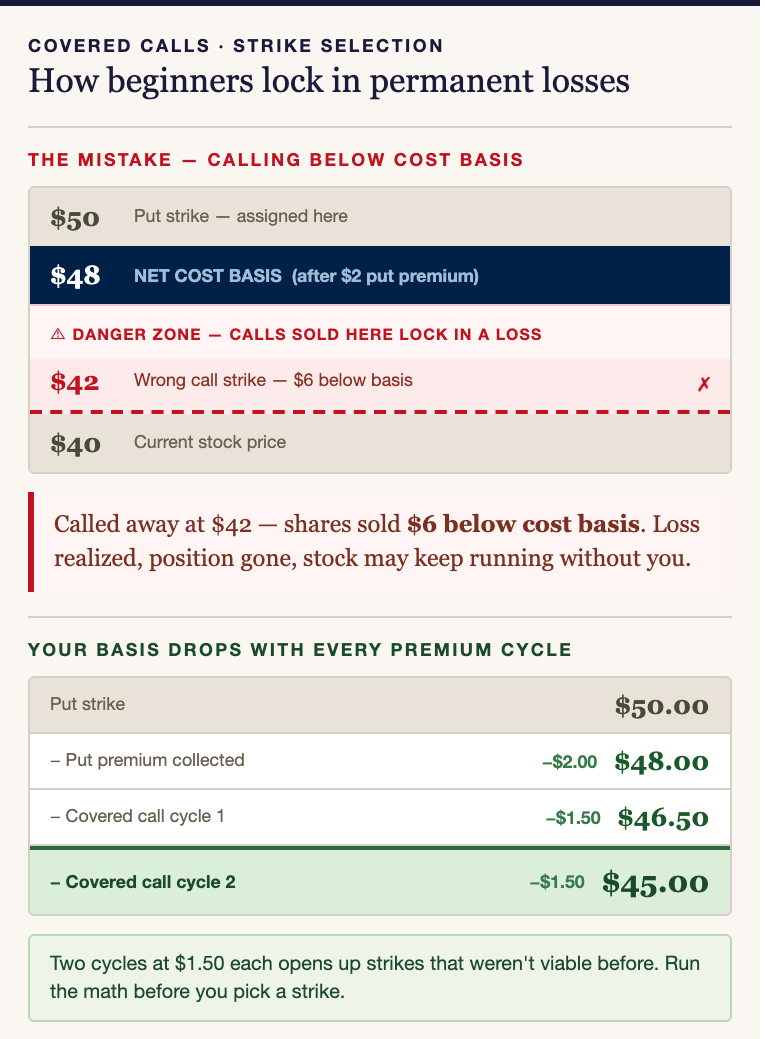

6. Selling Covered Calls Below Cost Basis

This is where beginners lock in permanent losses.

You got assigned at $50, collected $2 in premium — cost basis $48. Stock is now at $40. You want income, so you sell the $42 call. Stock rallies, you get called away at $42. You’ve just sold shares $6 below your cost basis. Loss realized, position gone, and the stock may keep running without you.

What most beginners miss: your real cost basis drops with every premium cycle.

Put strike ($50) minus put premium ($2) minus call premiums collected since assignment. Two covered call cycles at $1.50 each brings your real cost basis down to $45 — which opens up strikes that weren’t viable before. Run the math before you pick a strike.

If no strike at or above your cost basis pays meaningful premium, don’t sell a call this cycle. Wait. Patience in Phase 2 beats locking in a loss for the sake of collecting something.

The fix:

Calculate your real cost basis — put strike minus put premium minus all call premiums collected since assignment.

Only sell calls at or above that number.

No acceptable strike? Skip the cycle. Sitting on shares beats selling yourself into a realized loss.

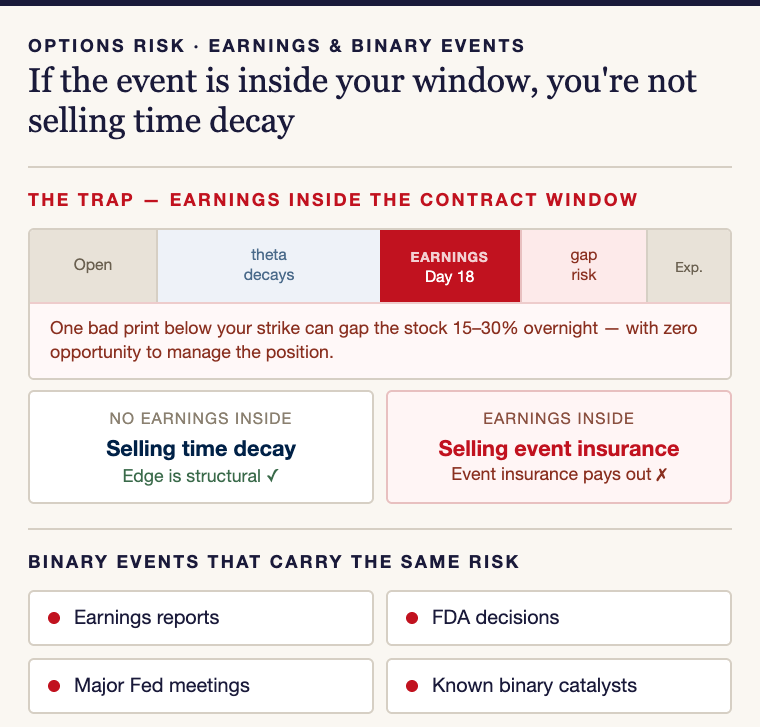

7. Wheeling Through Earnings and Binary Events

Pre-earnings IV is elevated for a reason. It’s the market pricing the actual move the stock is likely to make — and unlike the broad-market volatility risk premium, pre-earnings IV on individual stocks is often earned. The gap actually happens.

A stock that moves 8-12% after earnings three quarters out of four is going to keep doing that. One bad print below your strike can gap you 15-30% overnight with zero opportunity to manage the position.

Same logic applies to FDA decisions, major Fed meetings, and any known binary catalyst. If the event falls inside your contract window, you’re not selling time decay. You’re selling event insurance. Event insurance frequently pays out.

The fix:

Check the earnings calendar before opening any position

If earnings, an FDA date, or another binary event falls inside the expiration window: either close before the event or pick a strike that survives the stock’s worst historical earnings move

Every mistake on this list shares the same root: chasing premium instead of running good process.

Oversizing, trading high-IV junk, rolling forever, selling calls below cost basis — all of it traces back to optimizing for the credit rather than the trade. The premium is a byproduct. It follows from picking the right stock, the right strike, the right size, and the right timing. When you chase it directly, you take on risks the strategy wasn’t designed to carry.

The fix is always the same: slow down, size properly, pick quality names, and let the strategy compound at its own pace.

Knowing the Wheel Strategy and running it week after week are different problems.

The paid tier is where the system runs: fifteen setups every Monday with full management plans for every position, a printable PDF, and ten pre-filtered cash-secured puts every trading day.

The full breakdown is on the page below.

Since we're only selling cash-secured puts, why would we not have enough cash to cover all our assigned puts? Wouldn't a 5% cash reserve be enough to cover commissions, fees and any other transactional costs? Do you have any worst-case examples to illustrate when a 20% buffer is needed to cover assignment costs?

B